Creating a feasible financial plan and ensuring unwavering commitment to its implementation can often seem like an insurmountable task. Navigating the labyrinth of personal finance requires careful consideration, shrewd decision-making, and unwavering dedication. In this guide, we will explore the essential strategies to cultivate a practical budget and stay resolute in your financial pursuits.

Wise individuals understand that constructing a comprehensive and viable financial plan is not limited to mere numbers and calculations. It delves deep into identifying your financial aspirations, nurturing a resilient mindset, and embracing fiscal responsibility. With astute planning and unwavering resolve, you can shape a future that aligns with your dreams and provides a solid foundation for your financial well-being.

Revolutionize Your Health & Lifestyle!

Dive into the world of Ketogenic Diet. Learn how to lose weight effectively while enjoying your meals. It's not just a diet; it's a lifestyle change.

Learn MoreAssessing your current financial status is the first step towards developing an effective budget. By scrutinizing your income, expenses, and debts, you gain invaluable insights into your spending habits and financial priorities. Through this introspection, you can identify potential areas for improvement, set realistic goals, and embark on a journey towards financial freedom and stability.

Implementing your budget entails judicious decision-making and finding the perfect balance between short-term gratification and long-term financial security. Prioritize your expenses, differentiate between wants and needs, and imbue each monetary decision with a greater sense of purpose. By cultivating a discerning eye for financial opportunities and embracing frugality, you will forge a path towards sustainable wealth and personal fulfillment.

- Understanding the Importance of Budgeting

- Why Budgeting is Essential

- Managing Expenses

- Achieving Financial Goals

- Creating a Realistic Budget: Essential Steps to Financial Success

- Assess Your Current Financial Situation

- Determine Your Income and Expenses

- Set Realistic Financial Goals

- Create a Spending Plan

- Tips for Staying Committed to Your Budget

- Track Your Spending

- Questions and answers

Understanding the Importance of Budgeting

In today’s fast-paced world, it is crucial to have a clear understanding of the significance of budgeting. Effective budgeting is much more than just numbers on a spreadsheet or limiting your spending. It is a comprehensive financial plan that allows individuals and households to manage their income, expenses, debts, and savings in order to achieve financial stability and reach their long-term goals.

By creating and adhering to a budget, individuals can gain a deeper understanding of their financial situation and make informed decisions about how to allocate their resources. Budgeting provides a framework for setting realistic financial goals and enables individuals to track their progress towards these goals over time. Additionally, it helps to prioritize spending, ensuring that essential needs are met while also leaving room for personal enjoyment and experiences.

Moreover, budgeting plays a critical role in enabling individuals to manage debt effectively. By accurately tracking income and expenses, individuals can identify areas where they can cut back on spending and allocate more funds towards repaying debts. This can help them reduce interest payments and ultimately become debt-free sooner.

Furthermore, budgeting fosters a sense of control and empowerment over one’s finances. It allows individuals to take charge of their financial future and make informed decisions about how to best utilize their resources. By establishing clear financial goals and regularly monitoring their progress, individuals can make necessary adjustments and course corrections to stay on track towards achieving their objectives.

Budgeting also helps in building a strong financial foundation. By saving and investing wisely, individuals can build an emergency fund to navigate unexpected expenses, plan for major life events such as buying a home or starting a family, and secure a comfortable retirement. A well-planned budget ensures that individuals allocate a portion of their income towards savings, thus providing a safety net and greater financial security.

| Key Points |

| Understanding the importance of budgeting is essential for financial stability and achieving long-term goals. |

| Budgeting allows individuals to track their progress towards financial goals, prioritize spending, and effectively manage debt. |

| By budgeting, individuals can gain control over their finances, make informed decisions, and build a strong financial foundation. |

Why Budgeting is Essential

Understanding the significance of budgeting is vital for financial stability and success. It plays a crucial role in fulfilling our financial obligations, achieving our goals, and maintaining a balanced lifestyle. Budgeting entails intelligently distributing our income and resources to meet our needs, wants, and aspirations while ensuring a secure financial future.

Without a budget, managing our finances becomes challenging, and we may encounter unnecessary stress and financial strain. By creating and adhering to a budget, we gain clarity and control over our financial circumstances. It enables us to prioritize our spending, eliminate unnecessary expenses, and make informed financial decisions.

Moreover, budgeting facilitates the identification of our spending patterns and helps us understand where our money goes. It allows us to recognize areas where we may be overspending and develop strategies for reducing expenses and saving for future endeavors.

When we consistently follow a budget, we develop discipline and financial responsibility. We become more conscious of our financial choices and avoid impulsive spending. By embracing budgeting, we can eliminate debts, build an emergency fund, and work towards achieving our long-term financial goals, such as buying a home, starting a business, or planning for retirement.

In addition to the practical benefits, budgeting also promotes peace of mind and reduces financial anxiety. Having a clear financial plan in place gives us confidence in managing unexpected events and attaining financial independence. It empowers us to make intentional financial decisions and paves the way for a more secure and fulfilling future.

In summary, budgeting is essential because it provides us with the foundation for financial stability, independence, and success. By consciously managing our money, we can effectively control our spending, eliminate debts, save for the future, and achieve our financial aspirations. Embracing budgeting not only enhances our financial well-being but also brings peace of mind and reduces financial stress.

Managing Expenses

Controlling your spending and properly managing your expenses is an essential part of creating a successful budget and achieving your financial goals. By carefully considering how you allocate your money and making conscious choices about where to spend, you can ensure that your budget reflects your values and priorities.

One effective way to manage your expenses is by tracking your income and expenditures in a table. This allows you to have a clear overview of where your money is going and identify areas where you can make adjustments. By categorizing your expenses, such as housing, transportation, food, entertainment, and others, you can easily see which areas tend to consume the majority of your funds.

| Expense Category | Amount Spent |

|---|---|

| Housing | $1,200 |

| Transportation | $500 |

| Food | $400 |

| Entertainment | $300 |

| Other | $250 |

Once you have a clear understanding of your expenses, you can start evaluating which areas you can potentially cut back on. This could involve making small changes, such as reducing dining out expenses or finding more cost-effective alternatives for your everyday purchases. It is important to regularly review your expenses and make adjustments as needed to stay on track with your budgeting goals.

In addition to reducing expenses, it can also be helpful to consider ways to increase your income. This could be through taking on additional work or finding opportunities for side gigs. By boosting your income, you can have more financial flexibility and potentially allocate more funds towards your savings or debt repayment goals.

Managing expenses requires discipline and commitment. It may involve making tough choices and sacrifices in the short term in order to achieve long-term financial stability. However, by being mindful of your spending and continuously reassessing your financial habits, you can successfully manage your expenses and stay on track with your budget.

Achieving Financial Goals

Attaining desired financial milestones requires careful planning and dedication. This section explores effective strategies and approaches to help individuals achieve their financial goals. By implementing these techniques, individuals can enhance their financial well-being and secure a prosperous future.

|

1. Setting Clear Objectives |

Setting specific and measurable goals is the foundation for financial success. By clearly defining objectives, individuals can focus their efforts and make informed decisions that align with their aspirations. |

|

2. Embracing Smart Saving Techniques |

Saving money plays a crucial role in achieving financial goals. By adopting efficient saving strategies, individuals can build a financial safety net, establish emergency funds, and gradually accumulate wealth for future endeavors. |

|

3. Strategic Debt Management |

To achieve long-term financial goals, individuals must prudently manage their debt. By creating and following a well-structured debt payment plan, individuals can reduce interest costs, improve credit scores, and ultimately achieve financial stability. |

|

4. Enhancing Financial Literacy |

Developing a deep understanding of financial concepts and principles empowers individuals to make informed decisions about their money. By continuously educating themselves about personal finance, individuals can make wise investments and navigate financial markets with confidence. |

|

5. Seeking Professional Advice |

When facing complex financial decisions or uncertain circumstances, individuals can benefit from seeking guidance from qualified financial professionals. Their expertise can provide valuable insights and help individuals make sound choices that align with their goals. |

By following these strategies and incorporating them into their financial routines, individuals can cultivate a healthy financial mindset, maintain discipline, and work towards achieving their financial goals. Remember, each person’s journey is unique, and flexibility is key in adapting to changing circumstances along the way.

Creating a Realistic Budget: Essential Steps to Financial Success

Embarking on a journey toward financial stability and success begins with the creation of a realistic budget. By carefully planning and allocating your financial resources, you can gain control over your expenses, prioritize savings, and achieve your long-term financial goals. In this section, we will explore the crucial steps to follow when creating a practical budget that is tailored to your specific needs and aspirations.

|

Step 1: Identify Income and Expenses Start by comprehensively analyzing your income sources and categorizing them to gain a clear understanding of your overall financial inflow. Similarly, carefully scrutinize your expenses, ensuring to include both fixed and variable costs. This step will provide you with valuable insight into your spending patterns, enabling you to make more informed financial decisions. |

|

Step 2: Set Financial Goals Define your short-term and long-term financial goals, be it purchasing a house, saving for retirement, or paying off debts. By establishing specific goals, you can align your budgeting efforts with your aspirations and motivate yourself to stay committed to your financial plan. |

|

Step 3: Prioritize and Allocate Funds After gaining a clear understanding of your income, expenses, and financial goals, it’s time to allocate funds accordingly. Prioritize essential expenses such as housing, utilities, and transportation, and allocate a portion of your income towards savings. Consider cutting back on discretionary spending to ensure that your budget remains realistic and sustainable. |

|

Step 4: Track and Monitor Progress Creating a budget is just the beginning; it’s crucial to track and monitor your progress regularly. Use budgeting tools or apps to record your expenses, compare them to your allocated funds, and make necessary adjustments if needed. Constantly monitoring your budget will help you stay on track and make any necessary modifications to ensure financial success. |

|

Step 5: Reevaluate and Make Adjustments Life is dynamic, and circumstances change. Regularly reevaluate your budget and make necessary adjustments to cater to any new financial challenges or opportunities that may arise. This flexibility will allow you to maintain a realistic budget that adapts to your evolving needs while ensuring consistent progress towards your financial goals. |

By following these essential steps, you can create a practical and realistic budget that aligns with your financial needs and provides a solid foundation for long-term financial success. Remember, the key to budgeting is staying committed and regularly reviewing your progress to make informed financial decisions that will lead you closer to your desired financial future.

Assess Your Current Financial Situation

Gain a comprehensive understanding of your existing monetary status by evaluating your current financial circumstances. This crucial step involves analyzing various aspects of your financial position and determining its strengths and weaknesses.

Begin by examining your income sources, which may include wages, salaries, investments, and other means of earning. Identify the stability and consistency of your income streams to gauge your financial stability.

Next, assess your expenses, including both fixed and variable costs. Fixed expenses encompass regular payments like rent or mortgage, utilities, and insurance, while variable expenses include discretionary spending like dining out or entertainment. Evaluate your spending patterns and identify areas where you can potentially make adjustments to reduce unnecessary expenditures.

Additionally, it is essential to assess your current debt situation. Take stock of outstanding loans, credit card balances, and other liabilities. Determine your debt-to-income ratio to gauge your ability to manage and repay debts effectively.

Analyze your current savings and investment accounts to ascertain your level of financial preparedness for unexpected emergencies, such as medical expenses or job loss. Consider the returns on your investments and evaluate whether they align with your long-term financial goals.

Lastly, it is crucial to consider any future financial obligations you may have, such as upcoming major expenses or goals like purchasing a car, buying a home, or saving for retirement. By examining these factors, you can develop a clear picture of your financial situation and make informed decisions to create a realistic budget and achieve long-term financial stability.

Determine Your Income and Expenses

Assessing your financial situation involves understanding your sources of income and the various expenses that you incur on a regular basis. By examining both your income and expenses, you can gain a comprehensive overview of your financial standing and make informed decisions when creating a budget.

Begin by identifying all the different ways you earn money, including but not limited to your primary job, freelance work, rental income, and dividends from investments. It is crucial to consider all potential sources of income to have a holistic view of your financial inflows. Similarly, it is important to recognize and categorize your expenses, such as housing costs, transportation expenses, utility bills, groceries, entertainment, and any recurring payments or debts.

Take the time to analyze your income and expenses over a specific time period, such as a month or a quarter, to ensure accuracy. This will provide you with a clear understanding of your average income and expenses, helping you identify any patterns or fluctuations. Additionally, consider taking into account irregular or unexpected expenses, such as medical bills or car repairs, to account for potential financial surprises.

Once you have gathered all the necessary information, you can calculate your net income by subtracting your total expenses from your total income. This calculation will give you a realistic overview of how much money is available for budgeting and savings. It is essential to be honest and thorough during this step, as underestimating your expenses or overestimating your income can lead to unrealistic budgeting goals.

By determining your income and expenses, you will have a solid foundation for creating a realistic budget that aligns with your financial goals. Understanding your financial inflows and outflows allows you to make educated decisions about where to allocate your funds and prioritize your spending. Remember, regular reassessment of your income and expenses is necessary to ensure your budget remains accurate and effective.

Set Realistic Financial Goals

When it comes to managing your finances effectively, setting realistic financial goals plays a crucial role. By establishing clear objectives and targets, you can pave the way for financial success and create a roadmap to follow. These goals provide you with direction and motivation, helping you stay focused and committed to your financial journey.

Why are financial goals important? They give you a sense of purpose and enable you to prioritize your spending and saving habits. By setting achievable targets, you can break down your larger financial aspirations into smaller, more manageable steps.

Setting realistic financial goals requires a thorough assessment of your current financial situation. Take into account your income, expenses, debts, and any financial obligations you may have. Consider both short-term and long-term goals, ensuring they align with your financial capabilities and priorities.

It’s essential to be specific when setting financial goals. Instead of aiming for vague notions like saving money or becoming financially stable, define exactly what you want to achieve. For instance, you might set a goal to save a certain amount of money each month or pay off a specific debt within a set timeframe.

Once you’ve set your financial goals, it’s crucial to keep them in mind and track your progress regularly. Consider using tools such as budgeting apps or spreadsheets to monitor your expenditures and savings. Stay adaptable and flexible, adjusting your goals as necessary to accommodate changes in your financial circumstances.

Remember, setting realistic financial goals is about finding a balance between ambition and practicality. While it’s important to challenge yourself, setting unattainable goals can lead to frustration and demotivation. Be patient with yourself and celebrate small victories along the way.

In conclusion, setting realistic financial goals is an integral part of creating a successful financial plan. By clearly defining your objectives, you can stay committed to your budget, make informed financial decisions, and work towards a secure and prosperous future.

Create a Spending Plan

Developing a comprehensive spending plan is an essential part of managing your finances effectively. This section will provide guidance on how to strategically allocate your financial resources to meet your needs and goals.

Design a Financial Roadmap

First and foremost, it is crucial to design a financial roadmap that aligns with your long-term objectives. This involves identifying your financial goals, both short-term and long-term, and determining the resources required to achieve them.

Establish Priorities

Next, establish priorities for your spending plan. Identify the essential expenses that are necessary for basic living needs, such as housing, utilities, and food. Additionally, consider your financial responsibilities, such as loan repayments, insurance premiums, and savings contributions.

Allocate Discretionary Spending

After accounting for essential expenses and financial responsibilities, allocate a portion of your budget for discretionary spending. This allows you to enjoy leisure activities and indulge in non-essential purchases while still maintaining financial stability.

Track Your Spending

Consistently tracking your spending is a vital component of maintaining a successful spending plan. Use a budgeting tool or app to monitor your expenses and ensure that you are sticking to the allocated amounts for each category.

Monitor and Adjust

Regularly monitor your spending and make adjustments as needed. Over time, you may find that certain spending areas need to be reduced or reallocated to better align with your financial goals. Being flexible and open to modifications will contribute to your long-term financial success.

By creating a well-thought-out spending plan, you can confidently manage your finances, prioritize your needs and goals, and ultimately achieve financial stability.

Tips for Staying Committed to Your Budget

Ensuring the long-term success of your financial plans requires a steadfast commitment to your budget. It is essential to stay focused and motivated, even when facing unexpected expenses or temptations to overspend. By employing these tips, you can maintain your commitment to your budget and achieve your financial goals.

1. Remain mindful of your priorities: Regularly remind yourself of the reasons behind creating and sticking to a budget. Whether it’s saving for a dream vacation or becoming debt-free, keeping your goals in mind can help strengthen your commitment.

2. Track your spending: Continuously monitor your expenses to ensure you are staying within your budget. Pay careful attention to areas where you tend to overspend and find ways to make necessary adjustments to stay on track.

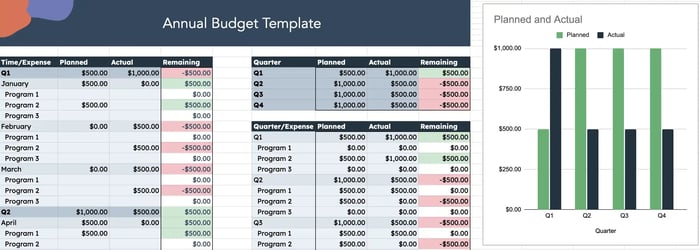

3. Utilize visual aids: Create visual reminders of your financial goals and progress. This could be a chart, a graph, or even a vision board that represents the things you hope to achieve by sticking to your budget. Place these visual aids where you will see them regularly to help maintain your commitment.

4. Seek support: Share your budgeting journey with trusted friends or family members who can provide encouragement and accountability. Consider joining online communities or forums dedicated to personal finance where you can connect with like-minded individuals who can offer support and guidance.

5. Celebrate milestones: Reward yourself when you achieve certain milestones in your financial journey. Recognize the progress you’ve made and find ways to celebrate without breaking your budget. This will help you stay motivated and focused on your long-term goals.

6. Develop healthy spending habits: Cultivate a mindset of conscious spending by evaluating each purchase against your budget and financial goals. Before making a purchase, ask yourself if it aligns with your priorities and if it’s necessary. By practicing mindful spending, you’ll be less likely to deviate from your budget.

7. Embrace the occasional splurge: While it’s essential to adhere to your budget, allowing yourself the occasional small splurge can help you stay committed in the long run. Set aside a designated amount in your budget for discretionary spending, giving yourself the freedom to enjoy occasional treats without derailing your financial plans.

8. Stay adaptable: Recognize that life can be unpredictable, and unexpected expenses or changes in circumstances may require adjustments to your budget. Instead of viewing these adjustments as failures, approach them as opportunities to learn and grow. Be flexible and willing to adapt your budget as needed.

9. Find joy in saving: Shift your mindset and find joy in saving rather than spending. Each time you add to your savings account or reach a financial goal, take a moment to appreciate the progress you’re making. This shift in perspective can help reinforce your commitment to your budget.

10. Practice self-discipline: Ultimately, staying committed to your budget requires self-discipline. Be mindful of your spending habits, avoid impulse purchases, and prioritize long-term financial success over short-term gratification. Remember that each small decision contributes to your overall financial well-being.

By implementing these tips and strategies, you can strengthen your commitment to your budget and navigate any challenges that may arise along the way. Stay focused, stay motivated, and keep your eyes on the financial future you are actively creating.

Track Your Spending

Monitoring your expenditures is a vital component of effectively managing your finances and achieving financial stability. Keeping a close eye on your spending habits allows you to gain insight into the areas where you may be overspending or could make cost-saving adjustments. By diligently tracking your expenses, you can make informed financial decisions and stay on track towards your budgeting goals.

One effective method of tracking your spending is by creating a comprehensive table that categorizes your expenses. Begin by listing different expense categories such as housing, transportation, groceries, entertainment, and miscellaneous. Within each category, further break down your expenses to provide more detailed information. For example, under the groceries category, you could include subcategories such as fruits and vegetables, dairy products, and snacks. This level of detailed tracking enables you to identify specific areas where you may need to cut back or allocate more funds.

| Expense Category | Subcategories | Amount Spent |

|---|---|---|

| Housing | Rent | $1000 |

| Transportation | Gas | $50 |

| Groceries | Fruits and Vegetables | $75 |

| Groceries | Dairy Products | $40 |

| Entertainment | Movie Tickets | $20 |

| Miscellaneous | Personal Care | $30 |

It is important to regularly update your spending table as soon as you make a purchase or incur an expense. This way, you can maintain an accurate record and have a clear overview of your spending patterns. Consider using a mobile app or spreadsheet to make this task more convenient and accessible. Additionally, be sure to review your spending table on a weekly or monthly basis to analyze your expenses and identify areas for improvement.

Tracking your spending allows you to be more conscious of where your money is going and helps you make informed decisions. By diligently recording your expenses and regularly reviewing your spending habits, you will be better equipped to stay committed to your budget and achieve your financial goals.

Questions and answers

How can I create a realistic budget?

Creating a realistic budget starts with determining your income and expenses. Track your spending habits for a month and categorize your expenses. Take into account your fixed expenses like rent or mortgage payments, utilities, and loan payments. Then, analyze your discretionary spending and prioritize your needs over wants. Set realistic saving goals and allocate a portion of your income towards savings. Finally, monitor and adjust your budget regularly to stay on track.

What are some tips to stay committed to my budget?

Staying committed to your budget requires setting achievable goals. Break down your goals into smaller, more manageable steps. Avoid impulsive purchases and make a habit of always consulting your budget before making any non-essential purchases. Consider using cash or a budgeting app to track your spending in real time. Find motivation by reminding yourself of the long-term benefits of sticking to your budget, such as financial independence and reduced debts.

How often should I review and adjust my budget?

It is recommended to review and adjust your budget on a monthly basis. This allows you to assess the effectiveness of your budget and make necessary changes. During the review, track your actual spending against your budgeted amounts to identify areas where you may be overspending or underspending. Evaluate any changes in your income or expenses and adjust accordingly. Regularly reviewing and adjusting your budget ensures that it remains realistic and aligned with your financial goals.

What are some common budgeting mistakes to avoid?

Some common budgeting mistakes to avoid are underestimating expenses, failing to allocate funds for unexpected costs, and not accounting for irregular, non-monthly expenses such as annual subscriptions or car maintenance. Another mistake is setting unrealistic saving goals or neglecting to save altogether. It is also important to avoid comparing your financial situation to others, as this can lead to overspending or unnecessary financial stress. Lastly, be aware of the temptation to rely on credit cards or loans to fund your budget.

How can I effectively track my expenses?

Effective expense tracking can be achieved through various methods. One way is to keep a daily record of all your expenses, whether it’s through a mobile app or a traditional pen-and-paper system. Categorize your expenses into different groups, such as groceries, transportation, entertainment, etc. Another option is to utilize online budgeting tools or software that automatically sync with your banking transactions. This allows you to have a clear overview of your spending habits and easily identify areas where you can cut back.

What are the first steps to creating a realistic budget?

The first steps to creating a realistic budget include gathering financial information, tracking expenses, setting financial goals, and determining income.

How can I track my expenses effectively?

You can track your expenses effectively by keeping receipts, using budgeting apps or spreadsheets, categorizing expenses, and reviewing your spending regularly.

Why is it important to set financial goals when creating a budget?

Setting financial goals is important when creating a budget because it gives you something to work towards, helps prioritize spending, and motivates you to stick to your budget.

What can I do to stay committed to my budget?

To stay committed to your budget, you can involve an accountability partner, automate savings, reward yourself for reaching milestones, and remind yourself of the long-term benefits of financial discipline.

How often should I review and adjust my budget?

It is recommended to review and adjust your budget on a monthly basis or whenever there are significant changes in your financial situation, such as a change in income or unexpected expenses.