Embarking on the journey towards achieving financial stability and independence is a profound endeavor that requires careful navigation and wise decision-making. With countless strategies and approaches available, it can be daunting to find the most effective path to financial success.

This comprehensive article aims to equip you with the top ten game-changing techniques for effectively managing your finances, allowing you to build a solid foundation for your future. By implementing these proven strategies, you can empower yourself to make informed financial decisions, maximize your wealth, and create a secure financial future.

Revolutionize Your Health & Lifestyle!

Dive into the world of Ketogenic Diet. Learn how to lose weight effectively while enjoying your meals. It's not just a diet; it's a lifestyle change.

Learn MoreThroughout this guide, we will explore a myriad of approaches to money handling, steering away from the conventional wisdom and delving into innovative and impactful methods. From adopting mindful spending habits to leveraging the power of technology, each strategy highlighted is designed to bring you closer to your financial aspirations.

Discover the art of financial intelligence, as we dive deep into the importance of budgeting, investing, and living within your means. Learn how to harness the potential of long-term investments and navigate the world of personal finance with confidence.

Unlock the secrets of successful wealth management, as we explore the significance of diversification, setting realistic goals, and making strategic choices to optimize your financial portfolio. Whether you’re just starting your journey or looking to enhance your existing financial prowess, this guide is a valuable resource that will undoubtedly reshape the way you approach money management.

- 10 Effective Approaches for Efficiently Managing Your Finances

- Create a Budget

- Understanding Your Earnings and Expenditures

- Setting Clear Financial Objectives

- Track Your Spending

- Identify Your Spending Habits

- Find Areas to Cut Back

- Build an Emergency Fund

- Save for Unexpected Expenses

- Ensure Financial Security

- Pay Off High-Interest Debt

- Questions and answers

10 Effective Approaches for Efficiently Managing Your Finances

Discovering methods to effectively handle your financial resources is an essential step toward achieving stability and prosperity. This section outlines ten strategies that can help you develop solid money management skills, secure your financial future, and improve your overall economic well-being.

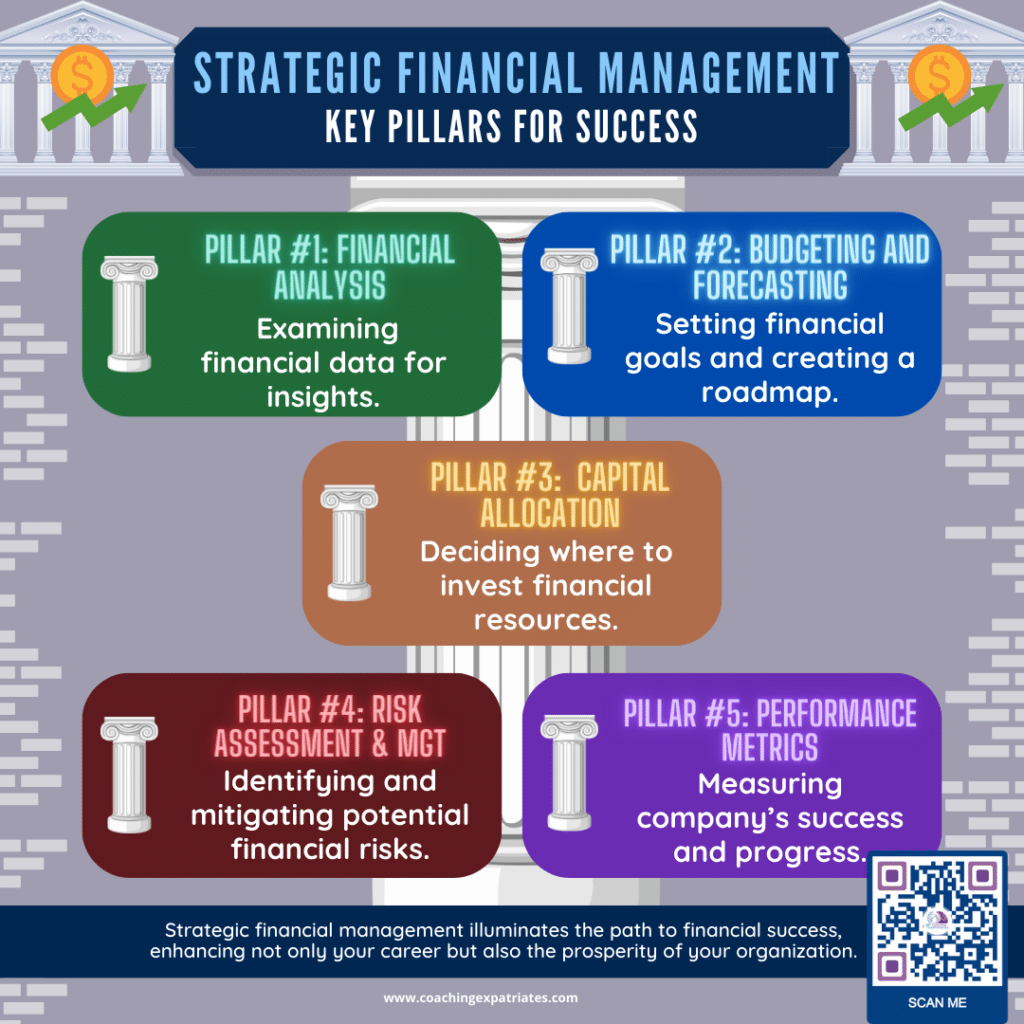

1. Financial Planning: Crafting a comprehensive financial plan is crucial for reaching your monetary objectives. It involves assessing your current financial standing, defining your goals, and formulating a feasible roadmap.

2. Budgeting: A well-structured budget acts as a foundation for financial success. It provides a clear overview of your income and expenses, ensuring that you prioritize essential expenditures and allocate funds accordingly.

3. Savings and Investments: Building a disciplined savings and investment strategy helps you create a safety net for emergencies and secure a stable future. Diversifying your investments and exploring various options can maximize potential returns.

4. Debt Management: Effectively managing debt is fundamental for maintaining a healthy financial profile. Establishing a repayment plan, consolidating debts, and avoiding unnecessary borrowing are key elements in this process.

5. Smart Spending: Adopting prudent spending habits allows you to make the most of your income. Differentiating between wants and needs, comparing prices, and seeking cost-effective alternatives are strategies that can help you optimize your expenses.

6. Building an Emergency Fund: Unexpected expenses can disrupt your financial stability. By establishing an emergency fund, you can cushion yourself from such situations and avoid falling into debt during times of crisis.

7. Insurance Coverage: Protecting your assets and loved ones through appropriate insurance coverage is an integral part of a comprehensive money management strategy. Depending on your circumstances, consider options such as life insurance, health insurance, and property insurance.

8. Regular Financial Monitoring: Keeping track of your income, expenses, and financial progress is essential for staying on top of your monetary affairs. Regularly reviewing your bank statements, monitoring your credit score, and reassessing your financial plan can help you stay in control.

9. Continual Education: The financial landscape is constantly evolving, making ongoing education vital for effective money management. By staying informed about new investment opportunities, tax strategies, and financial trends, you can refine your financial decision-making skills.

10. Seeking Professional Advice: At times, it may be beneficial to seek guidance from financial professionals. Getting support from experts who can provide personalized advice based on your unique circumstances can further enhance your money management strategies.

By implementing these ten money management strategies, you can gain a deeper understanding of your financial situation and make informed decisions that lead you towards a more stable and prosperous future.

Create a Budget

Developing a budget is an essential step towards achieving financial stability and control over your money. By creating a budget, you can effectively plan and allocate your income, expenses, and savings, enabling you to make informed financial decisions.

Start by analyzing your current financial situation and understanding your income sources. This includes your salary, bonuses, freelancing gigs, or any other sources of income. After identifying your income, it is crucial to determine your expenses and categorize them into fixed expenses, such as rent and utilities, and variable expenses, like groceries and entertainment.

Once you have a clear picture of your income and expenses, it is time to set financial goals. These goals can range from short-term objectives, such as saving for a vacation or paying off debt, to long-term goals like purchasing a house or planning for retirement. Your budget should align with these goals, outlining the necessary steps and adjustments required to achieve them.

- Track your expenses diligently: Keep a record of all your expenses, no matter how small. This will help you identify areas where you can potentially cut down costs and allocate your money wisely.

- Create spending categories: Divide your expenses into categories, such as housing, transportation, groceries, and entertainment. This will help you understand how much you are spending in each area and make adjustments if necessary.

- Set limits and prioritize: Determine how much you can allocate towards each spending category based on your income and financial goals. Prioritize essential expenses and be mindful of discretionary spending.

- Consider savings and emergencies: Ensure that your budget includes a provision for savings, both for short-term goals and emergencies. Building an emergency fund acts as a safety net during unexpected situations, providing you with financial security.

- Regularly review and adjust: Keep track of your budget regularly and make adjustments as needed. Life circumstances, income changes, or fluctuating expenses may require you to modify your budget over time.

In conclusion, creating a budget is a fundamental strategy for effective money management. It empowers you to take control of your finances, make informed decisions, and work towards achieving your financial goals. By diligently tracking your expenses and consciously allocating your income, you can pave the way for financial success and secure a stable future.

Understanding Your Earnings and Expenditures

Having a thorough comprehension of your income and expenses is fundamental to achieving financial stability. By gaining insight into your earnings and expenditures, you can make informed decisions and effectively manage your finances.

Begin by evaluating your sources of income, including salaries, wages, bonuses, or any additional revenue streams. It is crucial to comprehend the various forms of income and their consistency to ensure financial predictability.

Equally important is understanding your expenses, which consist of both essential and discretionary costs. Essential expenses are the necessary financial obligations, such as housing, utilities, transportation, and healthcare. Discretionary expenses, on the other hand, are discretionary spending choices, such as entertainment, dining out, and vacations. Being aware of your expenditure patterns enables you to prioritize and control your discretionary spending.

To gain a comprehensive understanding of your income and expenses, it can be helpful to create a detailed budget. A budget allows you to track and categorize your income and expenses accurately, enabling you to recognize areas where you can save or allocate funds strategically.

| Income | Expenses |

|---|---|

| Earnings from employment | Housing |

| Investment returns | Utilities |

| Rental income | Transportation |

| Freelance projects | Healthcare |

| Dividends | Essential groceries |

| Discretionary spending |

Regularly analyzing and reviewing your income and expenses empowers you to make adjustments to your financial strategy when necessary. It allows you to identify potential areas of improvement, such as reducing unnecessary expenses and seeking additional income sources.

An accurate understanding of your income and expenses serves as the foundation for effective financial management. In the next sections, we will explore strategies that can help you optimize your financial well-being based on this understanding.

Setting Clear Financial Objectives

Defining and setting clear financial goals is a crucial step towards achieving long-term financial success. By establishing specific objectives for your financial future, you can create a roadmap that will guide you towards financial stability and prosperity.

When you set clear financial goals, you are essentially creating a blueprint for your monetary aspirations. It involves identifying and articulating what you want to accomplish financially, whether it’s saving for retirement, purchasing a home, starting a business, or paying off debt. By clearly expressing your intentions, you can focus your efforts and make informed financial decisions that align with your desired outcomes.

Setting clear financial goals also provides you with a sense of purpose and motivation. It gives you something concrete to strive for and enables you to stay disciplined and committed to your financial journey. When you have well-defined objectives, it becomes easier to prioritize your spending, save effectively, and make wise investment choices.

Track Your Spending

Keep a record of your expenses and monitor where your money goes to gain control over your finances. Tracking your spending allows you to have a clear understanding of your financial habits and make better decisions about your money. By recording and categorizing your expenses, you can identify areas where you may be overspending or allocate your funds more effectively.

- Document your daily expenses: Make it a habit to record every expense you make, no matter how small. This includes purchases made with cash, credit cards, or online transactions.

- Categorize your expenses: Group your spending into different categories such as groceries, transportation, housing, entertainment, and others. This will help you identify which areas of your budget are consuming a large portion of your income.

- Use budgeting tools: Take advantage of budgeting apps or software that can automatically track your expenses and categorize them for you. This eliminates the need for manual record-keeping and makes it easier to analyze your spending patterns.

- Analyze your spending patterns: Regularly review your spending records to identify trends and patterns. This can help you understand your financial behavior and make adjustments accordingly.

- Set savings goals: Knowing how much you spend in different areas can help you set realistic savings goals. By tracking your expenses, you can identify areas where you can cut back and allocate more money towards savings or investments.

- Avoid impulse purchases: Reviewing your spending records can make you more mindful of impulsive buying habits. Being aware of your tendencies can help you resist the temptation to make unnecessary purchases.

By tracking your spending, you gain valuable insights into your financial habits and become more conscious of your money choices. It is an essential step towards achieving financial stability and success.

Identify Your Spending Habits

In order to achieve financial success, it is crucial to have a clear understanding of your personal spending habits. Recognizing and analyzing how you manage your finances can give you invaluable insights into your financial decisions and enable you to make necessary adjustments for a more secure future.

Take the time to reflect on your spending patterns and observe how you allocate your income. Understanding your financial habits involves looking at both the big picture and the smaller details, such as your daily expenses, monthly bills, and even occasional splurges.

By closely examining your spending tendencies, you can identify areas where you may be overspending or wasting money unnecessarily. It is important to be honest with yourself when analyzing these habits and be open to making changes that will benefit your long-term financial well-being.

Consider keeping a spending journal or using budgeting apps that can help you track and categorize your expenses. This will allow you to see where your money is going and identify any patterns or trends that may be hindering your financial progress.

Another aspect of identifying your spending habits is recognizing the emotions and triggers that influence your financial decisions. Whether it’s stress, boredom, or the desire to keep up with others, understanding the motivations behind your spending can provide valuable insights for making more conscious and informed choices.

By acknowledging and evaluating your spending habits, you can take the necessary steps to create a more balanced and efficient approach to managing your finances. This self-awareness will put you on the path towards financial stability and empower you to make more informed decisions regarding saving, investing, and achieving long-term financial success.

Find Areas to Cut Back

Identifying and reducing unnecessary expenses is an essential step towards achieving financial stability. By examining your spending habits and finding areas where you can minimize costs, you can create more opportunities for long-term financial success.

One effective approach is to closely analyze your monthly budget and identify any discretionary expenses that can be modified or eliminated. This involves considering alternative options or cheaper alternatives for various aspects of your life, such as entertainment, dining out, or subscription services. By making some adjustments and prioritizing your needs over wants, you can free up funds that can be directed towards important financial goals.

Another smart strategy is to review your fixed expenses, such as housing, utilities, and transportation. Even though these costs seem non-negotiable, there may still be opportunities to save. For instance, you could explore refinancing options for your mortgage or seek out more cost-effective insurance policies. Additionally, you can consider carpooling or using public transportation instead of relying solely on your own vehicle to significantly reduce fuel and maintenance expenses.

It is also crucial to assess your spending patterns and identify any habits or behaviors that contribute to unnecessary expenses. This could include impulsive shopping, excessive dining out, or subscription services that are no longer utilized. By becoming aware of these patterns, you can actively work towards changing your mindset and adopting more mindful spending habits.

Furthermore, finding areas to cut back may involve reevaluating your lifestyle choices. This might include downsizing your living space, minimizing or eliminating costly hobbies or activities, or reducing your reliance on convenience products or services. Simplifying your life can not only lead to financial benefits but also enhance your overall well-being.

- Review your monthly budget and identify discretionary expenses that can be reduced or eliminated.

- Explore alternatives or cheaper options for entertainment, dining out, or subscription services.

- Consider refinancing options for housing and seek out cost-effective insurance policies.

- Reduce transportation expenses through carpooling or public transportation.

- Evaluate spending patterns and make changes to promote mindful spending.

- Reevaluate lifestyle choices and consider downsizing, minimizing costly hobbies, or reducing reliance on convenience products.

By implementing these strategies and finding areas to cut back, you can not only improve your financial situation but also develop a more conscious and sustainable relationship with money. This proactive approach will set you on the path towards long-term financial success.

Build an Emergency Fund

In the midst of life’s uncertainties, it is essential to establish a financial safety net that will shield you from unexpected setbacks. Building an emergency fund is a vital component of sound money management. This section explores the importance of having a contingency fund and offers practical tips on how to create and maintain it.

Save for Unexpected Expenses

In this section, we will explore the importance of setting aside funds for unforeseen circumstances. Life is full of surprises, and being financially prepared for unexpected expenses can provide you with peace of mind and stability. By diligently saving a portion of your income, you can create a safety net to handle any unexpected costs that may arise.

Building an emergency fund is a prudent financial strategy. This reserve can help you cover unexpected medical bills, car repairs, or sudden job loss. Establishing a habit of saving regularly will enable you to handle these situations without jeopardizing your financial well-being.

Creating a buffer: It is essential to set aside a portion of your income each month to create a buffer against unexpected expenses. By consistently saving even a small percentage, you can gradually accumulate a significant amount over time.

Protecting your financial stability: Having funds readily available for unexpected expenses can safeguard your financial stability. By having this safety net, you can handle emergencies without relying on credit cards or loans, which can lead to debt and financial stress.

Peace of mind: Knowing that you have savings for unexpected expenses can provide peace of mind. Instead of worrying about how you will manage if something unexpected occurs, you can focus on other aspects of your life with a sense of security.

Adapting to change: Life is unpredictable, and circumstances can change in an instant. By saving for unexpected expenses, you can adapt to new situations without experiencing significant financial setbacks. This flexibility is crucial in maintaining your overall financial well-being.

Empowering yourself: Saving for unexpected expenses gives you a sense of control over your finances. By being prepared, you become less vulnerable to unexpected challenges, allowing you to take charge and make informed decisions.

Future planning: Saving for unexpected expenses is not only about the present but also about securing your future. Building a solid financial foundation can help you achieve long-term goals and aspirations, such as buying a house or retiring comfortably.

In conclusion, saving for unexpected expenses is a fundamental aspect of effective money management. By creating a financial safety net, you can protect yourself against unforeseen circumstances, reduce financial stress, and empower yourself to navigate through life’s ups and downs with confidence.

Ensure Financial Security

Securing your financial future is a vital aspect of achieving long-term stability and peace of mind. To guarantee financial security, it is essential to implement effective strategies that promote wealth accumulation and protection.

Creating a solid financial foundation involves making informed decisions to safeguard your resources and maximize your earning potential. By diversifying your income sources and investing wisely, you can mitigate risks and enhance your financial security.

Developing a comprehensive budget is another crucial step towards financial security. By carefully tracking your expenses and setting realistic financial goals, you can better manage your finances and ensure you are on the right path towards long-term financial stability.

In addition, having an emergency fund is crucial in maintaining financial security. By setting aside funds to cover unexpected expenses or income disruptions, you can weather financial storms and avoid falling into debt during challenging times.

- Regularly saving a portion of your income is an essential habit for financial security. Whether it’s through a retirement account or other investment vehicles, accumulating savings allows you to build wealth and protect yourself from unforeseen circumstances.

- It is also important to stay informed about changes in the financial landscape and adapt your strategies accordingly. Keeping up with market trends and seeking professional advice can help you make informed decisions and adapt to evolving economic conditions.

- Insurance is an integral component of financial security. By acquiring appropriate insurance coverage, such as health insurance, property insurance, and life insurance, you can protect yourself and your loved ones from unexpected financial burdens.

- Furthermore, staying disciplined and avoiding unnecessary debt is crucial for long-term financial security. By managing your debt responsibly and only borrowing when necessary, you can maintain a healthy financial position and avoid falling into a cycle of debt.

- Lastly, continuously educating yourself about personal finance and developing strong financial literacy skills is essential for long-term financial security. Understanding concepts such as investing, budgeting, taxes, and financial planning empowers you to make informed financial decisions and optimize your financial well-being.

By incorporating these strategies into your financial management approach, you can ensure your financial security and work towards achieving your long-term goals.

Pay Off High-Interest Debt

One crucial step towards achieving financial stability is to prioritize the repayment of high-interest debts.

Avoiding the accumulation of excessive interest payments and reducing financial burdens can pave the way for a more secure and prosperous future. It is essential to develop a strategic plan to tackle high-interest debts systematically.

- Identify Your High-Interest Debts: Start by assessing all outstanding debts and determining the ones with the highest interest rates. These may include credit card balances, personal loans, or any other forms of debt that incur high-interest charges.

- Establish a Repayment Strategy: Once you have identified your high-interest debts, create a repayment strategy. Consider using the debt avalanche method, where you prioritize paying off debts with the highest interest rates first while making minimum payments on other debts.

- Implement Debt Consolidation: Debt consolidation can be a helpful option to simplify payment processes and potentially reduce interest rates. Explore opportunities for consolidating your debts into a single loan with a lower interest rate.

- Create a Budget and Reduce Expenses: To allocate more funds towards debt repayment, create a comprehensive budget that tracks your income and expenses. Look for areas where you can cut back on discretionary spending and redirect those savings towards paying off your high-interest debts.

- Consider Balance Transfers: If you have outstanding credit card balances with high-interest rates, investigate the option of transferring those balances to a credit card with a lower or zero percent introductory interest rate. This strategy can help save money on interest payments while accelerating debt repayment.

- Explore Debt Negotiation: In some cases, you may be able to negotiate with creditors or debt collectors to reduce the overall amount owed or negotiate a lower interest rate. Be prepared to present your financial situation honestly and negotiate favorable terms.

- Seek Professional Advice: If managing your high-interest debts becomes overwhelming or you require expert guidance, consider consulting with a financial advisor or credit counselor. They can provide personalized strategies and assistance based on your specific financial circumstances.

- Stay Committed and Motivated: Consistency is key when paying off high-interest debts. Stay motivated by celebrating small victories along the way and regularly reassessing your progress. Tracking improvements can boost motivation and keep you focused on achieving your financial goals.

- Avoid Taking on New High-Interest Debt: While repaying your existing debts, it is crucial to avoid incurring additional high-interest debt. Minimize the use of credit cards and focus on living within your means. Prioritize saving and consider building an emergency fund to prevent reliance on high-interest borrowing in the future.

- Monitor Your Credit Score: As you work towards paying off high-interest debts, regularly monitor your credit score. Successfully managing and eliminating debt can significantly improve your credit rating, opening doors to better financial opportunities in the long run.

By prioritizing the repayment of high-interest debts and implementing thoughtful strategies, you can pave the way towards financial freedom and achieve greater control over your financial future.

Questions and answers

How can creating a budget help with financial success?

Creating a budget allows you to track your income and expenses, giving you a clear idea of where your money is going. By knowing how much you’re spending and on what, you can make informed decisions about your finances. A budget helps you prioritize your spending, avoid unnecessary expenses, and save money for future goals, which ultimately leads to financial success.

Why is it important to save regularly?

Regular saving is essential because it allows you to build wealth over time. By consistently putting aside a portion of your income, you can create an emergency fund, save for future expenses (such as buying a house or retirement), and have financial security. Regular saving also helps develop a disciplined financial habit and reduces the reliance on credit or loans in times of need.

What is the significance of setting financial goals?

Setting financial goals provides a clear direction for your financial journey. It helps you stay focused and motivated to achieve specific milestones. Whether it’s paying off debt, saving for a down payment, or planning for retirement, having well-defined financial goals allows you to make better financial decisions and track your progress effectively, leading to long-term financial success.

How can automating finances help with money management?

Automating finances refers to setting up automatic transfers for bill payments, savings, and investments. By automating these processes, you ensure that your financial obligations are met on time, and a portion of your income is consistently saved or invested. This reduces the chances of missed payments or impulsive spending, making it easier to stick to your financial plan and achieve your financial goals.

What are the top 10 money management strategies?

The top 10 money management strategies include setting financial goals, creating a budget, tracking expenses, saving regularly, investing wisely, avoiding debt, reviewing insurance needs, planning for retirement, diversifying income sources, and seeking professional advice.

How can setting financial goals help in managing money effectively?

Setting financial goals helps in managing money effectively as it provides a clear direction and purpose for your finances. It allows you to prioritize your spending, save adequately, and make informed financial decisions to achieve your desired objectives.

What are the benefits of creating a budget?

Creating a budget helps in managing money by providing a clear overview of your income and expenses. It helps you identify unnecessary spending, track your progress towards financial goals, and make adjustments to ensure that your spending aligns with your priorities.

Why is it important to save regularly?

Saving regularly is important as it allows you to build an emergency fund, plan for future expenses, and achieve long-term financial goals. It provides a financial cushion in times of unexpected events and helps you secure your financial future.

Why should one seek professional advice for money management?

Seeking professional advice for money management is beneficial as professionals have expertise in financial planning, investment strategies, and tax considerations. They can provide personalized guidance, help you optimize your financial decisions, and maximize your chances of achieving financial success.