In today’s fast-paced world, we all aspire to live a comfortable and secure life without constantly worrying about our finances. Financial stability is a goal that many strive to achieve, but it often feels elusive and challenging. However, with the right guidance and determination, it is possible to attain financial freedom.

In this article, we will explore ten practical and proven methods to help you bolster your financial well-being. Expert insights and advice from seasoned professionals in the field will empower you with the tools and knowledge to make wise financial decisions, save money, and ultimately build a solid foundation for a prosperous future.

Revolutionize Your Health & Lifestyle!

Dive into the world of Ketogenic Diet. Learn how to lose weight effectively while enjoying your meals. It's not just a diet; it's a lifestyle change.

Learn MoreThroughout this article, you will uncover strategies that are straightforward, yet powerful, in their ability to transform your financial situation. These guidelines have been carefully curated to provide you with a comprehensive roadmap towards financial independence. By adopting these principles into your life, you will not only save money but also cultivate a positive mindset that will help you navigate the complex world of personal finance with ease.

Whether you are just beginning your journey towards financial stability or looking for ways to improve your current fiscal status, this article will provide you with invaluable insights to help you achieve your goals. So, let’s dive in and discover the secrets to saving money and securing your financial future!

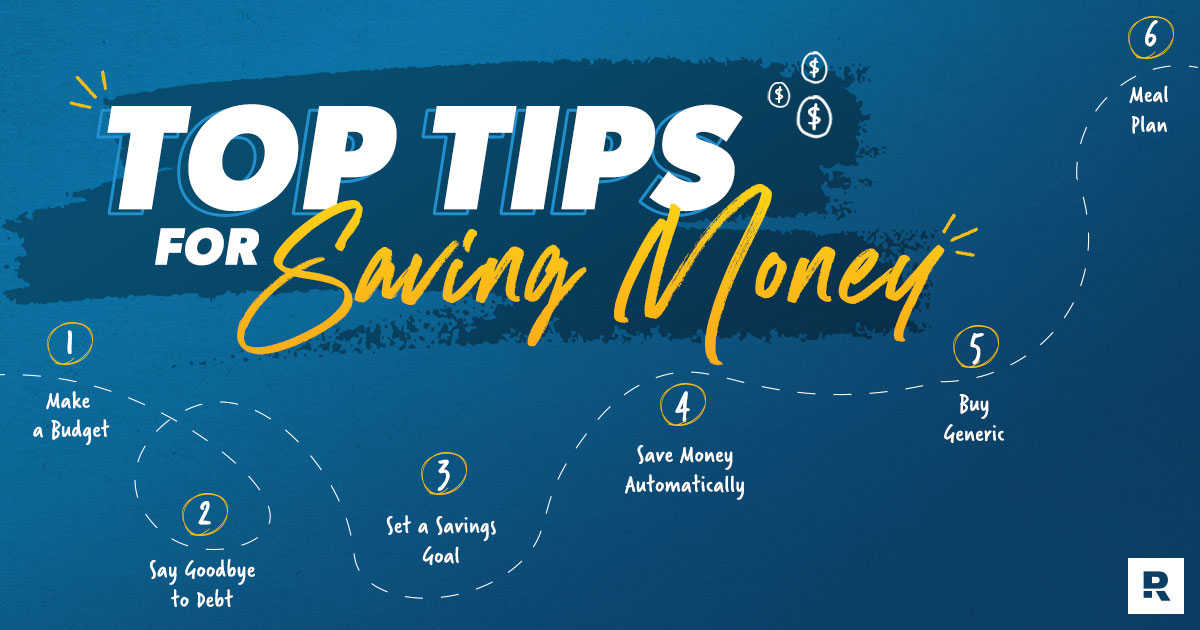

- Track Your Expenses

- Keep a Record of Every Penny Spent

- Identify Areas Where You Can Cut Back

- Create a Budget Tailored to Your Spending Habits

- Automate Your Savings

- Set Up Automatic Transfers to a Savings Account

- Start Small and Increase the Amount Over Time

- Make Saving a Priority Over Spending

- Cut Down on Unnecessary Expenses

- Cancel Unused Subscriptions and Memberships

- Reduce Dining Out and Take-Out Meals

- Find Cost-Efficient Alternatives for Entertainment

- Questions and answers

Track Your Expenses

Monitor Your Spending

One crucial step towards saving money is to have a clear understanding of your expenses. By tracking your expenses, you can gain insight into where your money is going and identify areas where you can cut back and save. Keeping a record of your spending habits allows you to take control of your finances and make informed decisions about your budget.

Keep Records of Your Purchases

One of the simplest ways to track your expenses is to keep a record of all your purchases. Whether it’s a small notebook, a dedicated app, or a spreadsheet, find a method that works for you and make it a habit to log every spending you make. By recording your purchases, you can easily review them and assess your spending patterns.

Categorize Your Expenses

Organizing your expenses into categories can help you analyze your spending habits more effectively. Break down your expenses into categories such as housing, groceries, transportation, entertainment, and others. This way, you can see exactly how much you’re spending on each category and identify areas where you might be overspending or where you could cut back.

Analyze Your Spending Patterns

Regularly reviewing and analyzing your expenses allows you to identify trends and patterns in your spending. Look for any unnecessary or impulsive purchases that you can eliminate. Consider setting spending limits for different expense categories to ensure that you stay within your budget.

Set Financial Goals

Tracking your expenses can also help you set and achieve financial goals. By being aware of where your money is going, you can make adjustments and allocate funds towards your savings or investments. Whether you’re saving for a vacation, a down payment on a house, or simply building an emergency fund, having a clear understanding of your expenses will help you stay on track towards reaching your financial goals.

Revisit and Revise Your Budget

Regularly reviewing your expenses will give you the opportunity to revise and adjust your budget accordingly. As your financial situation evolves, you may need to make changes to your spending habits and priorities. By tracking your expenses, you can ensure that your budget reflects your current financial goals and circumstances.

Keep a Record of Every Penny Spent

Track every single cent you spend, because these small expenses can add up over time. By keeping an accurate record of your spending, you can gain a clear understanding of where your money is going and identify areas where you can cut back.

Avoid the temptation to dismiss small expenses as insignificant – every penny counts. Writing down every purchase, no matter how small, will make you more mindful of your spending habits and help you make informed decisions about where to allocate your money.

Consider creating a simple table to record your expenses. Divide it into categories such as food, transportation, entertainment, and miscellaneous. This will provide you with a visual representation of how much you spend in each area and allow you to identify any patterns or areas for improvement.

Review your record regularly to identify any unnecessary expenses or places where you can make adjustments. For example, if you notice that you are spending a significant portion of your income on dining out, you can start planning and preparing meals at home more often to save money.

Keeping a record of every penny spent is a powerful tool that empowers you to take control of your finances. It allows you to make smarter decisions about how to spend your money, prioritize your expenses, and ultimately, save more in the long run.

| Category | Amount Spent |

|---|---|

| Food | $200 |

| Transportation | $100 |

| Entertainment | $50 |

| Miscellaneous | $75 |

Identify Areas Where You Can Cut Back

Discovering ways to reduce your expenses and allocate your funds wisely is crucial when it comes to achieving financial stability. By evaluating different aspects of your daily life, you can identify specific areas where you have the potential to decrease your spending without sacrificing your overall quality of life.

Start by closely examining your monthly bills and expenses, and take note of any recurring costs that may be higher than necessary. Look for opportunities to renegotiate contracts or switch providers, potentially saving significant amounts of money in the long run. Additionally, consider evaluating your spending habits and determining which areas could benefit from a more cautious approach.

One prominent area where many individuals can cut back is in their entertainment expenses. This may involve reducing the frequency of dining out or exploring alternative free or low-cost activities for leisure. By taking advantage of local parks, libraries, and community events, you can still enjoy yourself while avoiding unnecessary expenditures.

Another area to consider is your transportation costs. Evaluate your current mode of transportation and explore alternative options that may be more cost-effective. This could include using public transportation, carpooling, or even utilizing ride-sharing services instead of owning a personal vehicle.

Furthermore, it is important to examine your spending on non-essential items and impulse purchases. Consider implementing a wait-and-see approach, where you wait a certain period of time before making a purchase to determine the actual necessity or desire for the item. This can help prevent the accumulation of unnecessary expenses and create a more mindful approach to shopping.

Identifying areas where you can cut back requires a thoughtful analysis of your spending habits and a willingness to make necessary adjustments. By following these tips and taking proactive steps towards reducing expenses, you can effectively save money and improve your financial well-being.

Create a Budget Tailored to Your Spending Habits

Developing a budget that aligns with your unique spending patterns is an essential step towards achieving financial stability. To effectively manage your finances and save money, it is crucial to create a budget that reflects your individual needs and priorities. By understanding your spending habits and identifying areas where you can make adjustments, you can take control of your financial future.

Start by examining your monthly income and categorizing your expenses. This process will provide valuable insights into your spending patterns and help you identify areas where you can cut back. Consider organizing your expenses into different categories, such as housing, transportation, groceries, entertainment, and debt payments. Creating this structure will allow you to see where the majority of your money is going and where you might have opportunities to reduce costs.

Next, determine your financial goals. Whether you want to save for a down payment on a house, pay off existing debt, or build an emergency fund, having clear objectives will guide your budgeting decisions. Prioritize your goals and allocate a portion of your income towards each one. Remember to be realistic about what you can afford to save or invest each month to avoid unnecessary stress or strain on your budget.

Once you have a clear understanding of your income, expenses, and financial goals, it’s time to create a budgeting plan. Start by setting limits or caps on your spending in each category. This will ensure that you stay within your means and avoid overspending. Consider implementing strategies such as the envelope system, where you allocate a certain amount of cash to each spending category and only use that designated amount for the month.

Regularly monitor your budget and track your progress. Review your spending and saving habits on a weekly or monthly basis to identify any areas where you may need to make adjustments. Be flexible and willing to adapt your budget as needed. Life circumstances and financial goals may change, requiring you to modify your budget accordingly.

Creating a budget based on your spending habits takes time and effort, but it is a valuable tool to help you reach your financial goals. By understanding your income, expenses, and priorities, you can make informed decisions about where to allocate your funds and save money effectively.

Automate Your Savings

Streamline your savings process by automating it. This simple and effective method allows you to consistently set aside money without having to remember to do so manually. By utilizing automatic savings tools and features, you can effortlessly build your savings and achieve your financial goals.

One way to automate your savings is by setting up automatic transfers. This means arranging for a specific amount of money to be moved from your checking account to your savings account on a regular basis. Whether it’s a weekly, bi-weekly, or monthly transfer, this method ensures that you consistently contribute to your savings without any extra effort on your part.

Another option is to use automated savings apps or platforms. These innovative tools allow you to customize your savings goals and preferences, and they automatically allocate a portion of your income towards your savings. With features like round-up savings, where your purchases are rounded up to the nearest dollar and the difference is automatically transferred to your savings account, saving becomes effortless and almost invisible.

Additionally, consider signing up for direct deposit if it’s available to you. By having your paycheck automatically deposited into your savings account, you eliminate the temptation to spend that money before saving it. This method ensures that a portion of your income goes directly into your savings, making it easier to save consistently.

Automating your savings not only simplifies the process, but it also helps you overcome common obstacles to saving. It removes the need for willpower and discipline, as the process becomes automatic. Furthermore, automating your savings allows you to take advantage of the power of compounding interest over time, as your savings grow faster through regular contributions.

- Set up automatic transfers from your checking to savings account

- Explore automated savings apps or platforms

- Consider signing up for direct deposit

- Bypass the need for willpower and discipline

- Take advantage of the power of compounding interest

By automating your savings, you can consistently grow your financial resources and work towards your financial goals. This simple and effective method ensures that saving becomes a priority and a regular habit, ultimately leading to long-term financial security.

Set Up Automatic Transfers to a Savings Account

Streamline your savings strategy by implementing automatic transfers to a designated savings account. This convenient method allows you to effortlessly allocate a portion of your income towards savings on a regular basis.

By setting up automatic transfers, you create a consistent and disciplined approach to saving money. Rather than relying on sporadic manual deposits, automatic transfers ensure that a predetermined amount of funds is regularly allocated to your savings account, without requiring any additional effort on your part.

Not only does this method promote financial stability, but it also helps you to avoid the temptation of spending your disposable income before saving. By automatically allocating funds to your savings account, you cultivate the habit of prioritizing saving money, even if it means sacrificing immediate gratification.

Moreover, automatic transfers provide a sense of accountability, as they establish a fixed savings goal that you commit to achieving on a regular basis. This consistency will enable you to steadily build your savings over time, ultimately helping you reach your financial objectives.

Setting up automatic transfers is a straightforward process. Simply contact your bank or financial institution to inquire about their automatic transfer options. They will guide you through the necessary steps, allowing you to customize the frequency and amount of the transfers according to your financial goals and needs.

Remember, setting up automatic transfers to a savings account is an effective way to take control of your finances and build a solid foundation for future financial success.

Start Small and Increase the Amount Over Time

In the realm of personal finance, it is often said that every little bit counts. When it comes to saving money, starting small and gradually increasing the amount you save over time can have a significant impact on your financial well-being. By adopting this approach, you can build a strong foundation for long-term saving habits and achieve your financial goals.

Initially, it may seem challenging to set aside money for savings, especially if you have limited funds. However, even small contributions can make a difference. Begin by identifying areas where you can cut back on expenses or make small lifestyle changes. This could mean bringing homemade lunches to work instead of eating out, reducing your monthly subscription services, or finding lower-cost alternatives for your regular purchases.

- Create a budget and allocate a portion of your income towards savings. Start with a modest percentage, such as 5% or 10%, and progressively increase it as you become more comfortable with saving.

- Consider automating your savings. Set up automatic transfers from your paycheck or checking account to a separate savings account. This way, saving becomes a consistent and effortless habit.

- Take advantage of spare change and small amounts of cash. Designate a jar or container to collect loose change, and periodically deposit it into your savings account. These small amounts may not seem significant, but over time they can accumulate into a noteworthy sum.

- Keep track of your progress. Regularly monitor your savings and celebrate milestones along the way. This will not only motivate you to continue saving but also give you a sense of accomplishment.

- As you become more comfortable with saving, challenge yourself to increase the amount you set aside each month. Gradually raise the percentage or fixed amount, but ensure it remains within your financial capabilities.

Starting small and gradually increasing the amount you save over time is a sustainable approach to building wealth. By making consistent efforts to save, even if it’s just a small amount, you are developing good financial habits that will serve you well in the long run. Remember, the journey to financial stability begins with a single step, and every step counts.

Make Saving a Priority Over Spending

When it comes to managing your finances, it’s important to prioritize saving over spending. By making saving a top priority, you can ensure that you have a solid financial foundation for the future. Instead of focusing on immediate gratification through spending, shift your mindset towards long-term financial goals and the benefits of saving.

One approach to making saving a priority is to create a budget that includes a specific savings goal. Allocate a portion of your income towards savings each month and make it a non-negotiable expense. Treat saving as an essential bill that must be paid. By setting aside a predetermined amount regularly, you can gradually build your savings over time.

Another way to prioritize saving is to establish an emergency fund. Unexpected expenses can arise at any time, such as medical bills or car repairs. Having an emergency fund can help you avoid dipping into your savings or relying on credit cards to cover these expenses. Start small by saving a portion of your income each month until you have built up enough to cover three to six months’ worth of essential expenses.

Additionally, it’s important to resist the temptation of impulsive spending. Before making a purchase, ask yourself if it aligns with your financial goals and if it’s a necessity. Consider the long-term impact of your spending habits on your savings. Delaying gratification and practicing mindful spending can help you prioritize saving over unnecessary purchases.

Furthermore, avoid falling into the trap of consumerism and societal pressure to keep up with the latest trends. Instead of constantly chasing material possessions, shift your focus towards experiences and personal growth. Invest in personal development, education, or travel, which can bring long-lasting fulfillment without draining your savings.

| Key Points: |

|---|

| – Prioritize saving over spending |

| – Create a budget with a savings goal |

| – Establish an emergency fund |

| – Practice mindful spending |

| – Avoid consumerism and societal pressure |

Cut Down on Unnecessary Expenses

Reducing unnecessary expenditures is a crucial strategy in managing your finances wisely and achieving long-term financial stability. By identifying and eliminating unnecessary expenses, you can free up a significant portion of your income for more essential and meaningful purposes.

One effective way to reduce unnecessary expenses is to carefully evaluate your spending habits and identify any areas where you can make adjustments. This may involve cutting back on luxury purchases and focusing on essentials, such as housing, transportation, and groceries.

Another way to curb unnecessary expenses is to prioritize your needs over your wants. By distinguishing between essential expenses and discretionary spending, you can make more informed decisions about where to allocate your funds.

Furthermore, it is essential to resist the temptation of impulse buying. By practicing mindful spending and carefully considering your purchases before making them, you can avoid wasting money on items that provide little to no long-term value.

Additionally, assessing your subscriptions and memberships can also help in cutting down unnecessary expenses. Review the services you currently use and determine whether they are truly necessary. Consider canceling any subscriptions or memberships that you no longer find valuable or utilize.

Utilizing a budgeting system can also make a significant impact on reducing unnecessary expenses. By tracking your income and expenses, you can gain a clear understanding of where your money is going and identify areas where you can potentially save.

Lastly, periodically reevaluating your financial goals and priorities can help you stay motivated and make smarter financial decisions. By focusing on your long-term objectives, you can better resist the temptation of unnecessary expenses and work towards a more financially secure future.

Cancel Unused Subscriptions and Memberships

Reduce your expenses and maximize your savings by evaluating and canceling any subscriptions or memberships that you no longer use or need. By eliminating these unnecessary expenses, you can free up money for more essential purchases or put it towards achieving your financial goals.

Start by reviewing your bank statements or credit card bills to identify recurring charges for subscriptions or memberships. Take note of each item and consider whether you still derive value from them. Are they adding meaningful benefits to your life or enhancing your personal or professional growth?

Create a list of the subscriptions and memberships that you are currently paying for and evaluate each one individually. Consider factors such as the frequency in which you utilize the service, whether there are any cheaper alternatives available, and whether the benefits outweigh the costs. Be honest with yourself and recognize if some subscriptions or memberships are simply not worth the expense.

Once you have identified the subscriptions and memberships that you no longer need, it’s time to take action. Contact the service provider or organization and inquire about the cancellation process. Some may have online cancellation options, while others may require a phone call or written notice. Follow the necessary steps to cancel each one effectively.

As you go through this process, be mindful of any cancellation fees or penalties associated with terminating certain subscriptions or memberships before their contract term expires. Factor in these costs when making your decision, but don’t let them deter you if the long-term savings outweigh the upfront expense.

- Consider downgrading or seeking alternative options for subscriptions or memberships that you still find valuable but may be able to reduce in cost.

- Regularly review your expenses to ensure you are not unknowingly signing up for new subscriptions or memberships that may not align with your current needs.

- Use budgeting tools or apps to track your spending and identify any recurring charges that may have slipped your attention.

- Revisit your list of canceled subscriptions and memberships periodically to reassess whether you still feel confident in your decision.

By regularly evaluating and canceling unused subscriptions and memberships, you can maintain control over your finances and allocate your hard-earned money towards the things that truly matter to you.

Reduce Dining Out and Take-Out Meals

One effective strategy to save money is to cut down on the amount of money spent on dining out and ordering take-out meals. By reducing the frequency of eating out and opting for preparing meals at home, individuals can significantly reduce their expenses, allowing for greater financial stability and savings.

One of the primary advantages of reducing dining out is the potential for significant cost savings. Eating at restaurants and ordering take-out meals often comes at a premium price due to the additional costs involved in meal preparation, service, and overhead. By preparing meals at home, individuals can enjoy the same dishes at a fraction of the cost while having the opportunity to control the quality of ingredients used.

Additionally, cooking at home allows individuals to have better control over their portion sizes, leading to potential health benefits. Many restaurant meals and take-out options are often high in calories, unhealthy fats, and sodium, which could have long-term negative effects on both health and finances. By preparing meals at home, individuals can choose nutritious ingredients, control portion sizes, and tailor their meals to meet their dietary needs, thus promoting a healthier lifestyle.

Another way to reduce dining out expenses is to plan meals in advance. By creating a weekly meal plan and shopping for groceries accordingly, individuals can avoid spontaneous and costly trips to restaurants or ordering take-out due to lack of time or ideas for meals. Planning meals in advance also allows for more efficient use of ingredients and a reduction in food waste, which can further contribute to additional savings.

| Benefits of Reducing Dining Out and Take-Out Meals |

|---|

| 1. Cost savings |

| 2. Control over ingredients and portion sizes |

| 3. Potential health benefits |

| 4. Meal planning for efficiency |

In conclusion, reducing the frequency of dining out and relying less on take-out meals can have numerous benefits, including significant cost savings, better control over ingredients and portion sizes, potential health benefits, and improved meal planning efficiency. By making conscious choices to prepare meals at home, individuals can take control of their finances and work towards achieving their savings goals.

Find Cost-Efficient Alternatives for Entertainment

Looking for budget-friendly ways to have fun and entertain yourself? This section will explore various alternatives that won’t break the bank. It’s crucial to find affordable options for entertainment without compromising on enjoyment or quality. By considering these alternatives, you can discover new and exciting experiences while saving money.

| 1. Community Events: | Check out local community centers, parks, or cultural organizations for free or low-cost events. Many cities often host concerts, festivals, movie nights, and art exhibitions, offering a wealth of entertainment options without draining your wallet. |

| 2. Outdoor Activities: | Take advantage of natural surroundings and engage in outdoor activities such as hiking, cycling, or picnicking. Nature provides a serene and cost-effective backdrop to enjoy quality time with friends and family. |

| 3. DIY Projects: | Tap into your creative side and explore do-it-yourself projects. Whether it’s painting, crafting, or home improvement, engaging in DIY activities can be a fun and inexpensive way to entertain yourself while also enhancing your skills. |

| 4. Visit Local Libraries: | Libraries are treasure troves of entertainment. Borrow books, magazines, movies, or even attend author readings or workshops at the library. It’s an economical way to indulge in various forms of entertainment and expand your knowledge. |

| 5. Potluck Parties: | Instead of dining out or hosting expensive parties, organize potluck gatherings with friends and family. Each person can contribute a dish, making it a shared and affordable experience that still offers great food, company, and entertainment. |

| 6. Streaming Services: | Subscribe to streaming platforms that offer a wide range of movies, TV shows, and documentaries at a fraction of the cost of cable or satellite subscriptions. With numerous options available, you can find a streaming service that matches your preferences and budget. |

| 7. Utilize Coupons and Discounts: | Keep an eye out for coupons and discounts for various entertainment activities, such as movie tickets, theme parks, or concerts. Online deal websites, newsletters, and loyalty programs often offer significant savings for those who plan ahead. |

| 8. Explore Free Online Resources: | The internet provides a wealth of free entertainment options. Take advantage of podcasts, online tutorials, educational websites, and free e-books to learn new skills and indulge in your interests without spending a dime. |

| 9. Volunteer for Events: | Consider volunteering at events, concerts, or festivals. In exchange for your time and effort, you can often gain free entry or discounted tickets to enjoy the event. It’s a win-win situation, allowing you to support the community while enjoying entertainment. |

| 10. Local Clubs and Groups: | Join local clubs or groups that share common interests. From book clubs to sporting teams, these communities offer opportunities for social interaction and entertainment at minimal or no cost. |

With these cost-efficient alternatives for entertainment in mind, you can pursue your hobbies and interests without straining your budget. Remember, it’s all about finding enjoyable experiences that don’t compromise your financial goals.

Questions and answers

What are some simple ways to save money?

There are various simple ways to save money, such as creating a budget, cutting down on unnecessary expenses, and setting savings goals. Additionally, you can save money by cooking at home instead of eating out, using coupons and discount codes when making purchases, and negotiating lower bills for services.

Is it really effective to save money?

Absolutely! Saving money is highly effective as it allows you to have a financial safety net, achieve your financial goals, and have peace of mind during emergencies. By saving money, you can also gain financial independence and have more control over your future.

How can I save money if I have a low income?

Even with a low income, it is still possible to save money. You can start by tracking your expenses and cutting down on unnecessary spending. Look for ways to increase your income, such as taking up a side job or selling unwanted items. It’s also beneficial to save small amounts consistently and consider opening a savings account.

Are there any specific tips for saving money on groceries?

Yes, there are several ways to save money on groceries. First, make a shopping list and stick to it to avoid impulse purchases. Look for sales and discounts, buy in bulk for non-perishable items, and consider purchasing store brands instead of name brands. Planning meals in advance and using leftovers creatively can also help reduce food waste and save money.

Is it better to save money in a bank or invest it?

It depends on your financial goals and risk tolerance. Saving money in a bank, such as a savings account, offers security and easy access to your funds. However, the interest rates are usually low. Investing money in stocks, bonds, or other financial instruments can potentially yield higher returns but involves a level of risk. It is recommended to seek guidance from a financial advisor to determine the best approach based on your individual circumstances.

1. How can I save money on a tight budget?

One effective way to save money on a tight budget is by creating a financial plan and sticking to it. This involves tracking your expenses, identifying unnecessary expenses, and finding alternatives or cutting back on them. Additionally, you can look for ways to increase your income, such as taking on a side job or freelance work. It’s also important to prioritize your spending and distinguish between wants and needs.

2. Are there any specific tips on saving money on groceries?

Yes, there are several ways to save money on groceries. One tip is to make a shopping list before going to the store and stick to it to avoid impulse purchases. It’s also beneficial to compare prices at different stores, use coupons or discounts, and buy in bulk whenever possible. Additionally, planning your meals in advance can help you avoid food waste and save money.

3. What are some effective strategies for saving money on utilities?

There are various strategies you can implement to save money on utilities. Firstly, you can conserve energy by turning off lights and electronics when not in use, using energy-efficient light bulbs, and adjusting the thermostat to an optimal temperature. Installing low-flow showerheads and faucets can help save water. Additionally, insulating your home and sealing any drafts can reduce heating and cooling costs.

4. How can I save money on entertainment expenses?

To save money on entertainment expenses, you can explore free or low-cost activities, such as visiting local parks, attending community events, or taking advantage of free museum days. Instead of dining out or going to the movies, you can opt for cooking meals at home and having movie nights in. Another option is to consider sharing subscriptions or memberships with friends or family to reduce costs.

5. What are some long-term saving strategies?

Long-term saving strategies include setting financial goals, such as saving for retirement or a down payment on a house, and creating a budget that includes regular contributions towards these goals. It is also wise to explore investment options, such as opening a retirement account or investing in stocks or real estate, to grow your savings over time. Additionally, it’s important to regularly review and adjust your saving strategies based on your financial situation and goals.