Are you tired of struggling with your finances? Do you find yourself constantly worrying about how to make ends meet? It’s time to take charge of your financial future and create a solid foundation for success. In this article, we will guide you through five essential steps to develop a practical and effective financial plan that will change your life.

Step 1: Establishing a Clear Vision

Revolutionize Your Health & Lifestyle!

Dive into the world of Ketogenic Diet. Learn how to lose weight effectively while enjoying your meals. It's not just a diet; it's a lifestyle change.

Learn MoreImagine this: a life free from financial stress, where you can pursue your dreams and achieve your goals. Whether you want to pay off debt, save for a down payment on a house, or enjoy a comfortable retirement, having a clear vision will provide the motivation and direction you need to create a budget that works.

Take some time to reflect on your financial aspirations and write them down. Visualize what achieving those goals would mean for you and your loved ones. This exercise will help you stay focused and committed throughout the budgeting process.

Step 2: Assessing Your Current Financial Situation

Before you can map out your financial journey, it’s essential to have a complete understanding of where you stand. Take stock of your income, expenses, and debts. Analyze your spending habits and identify areas where you can make adjustments. This honest assessment will provide the insights needed to create a realistic budget that aligns with your financial goals.

- 5 Strategies for Crafting an Effective Financial Plan for Success [Your Website Name]

- Step 1: Assess Your Financial Situation

- Gather all financial documents

- Analyze your income and expenses

- Step 2: Set Clear Financial Goals

- Identify short-term and long-term goals

- Make your goals specific, measurable, attainable, relevant, and time-bound (SMART)

- Step 3: Develop a Feasible Spending Plan

- Track Your Income and Expenses

- Categorize your expenses and allocate a budget for each category

- Consider including savings and emergency funds in your budget

- Step 4: Implement and Monitor Your Spending Plan

- Questions and answers

5 Strategies for Crafting an Effective Financial Plan for Success [Your Website Name]

Building a solid financial strategy is crucial for attaining your goals and achieving long-term financial stability. By implementing a well-thought-out plan, you can confidently navigate the complexities of managing your money and make informed decisions that lead to a better future.

1. Establishing clear objectives: Before diving into the nitty-gritty details of your financial plan, it’s essential to define your objectives. Determine what you want to achieve in terms of savings, investments, debt reduction, or any other financial goals that are important to you. This step will provide you with a target to work towards and keep you motivated throughout the process.

2. Analyzing your income and expenses: To create an effective financial plan, you need a clear understanding of your cash flow. Evaluate your sources of income and calculate your regular expenses, including fixed and variable costs. By gaining insight into your spending habits and identifying areas where you can cut back, you can allocate your resources more effectively and save for the future.

3. Crafting a realistic budget: A budget is the backbone of any successful financial plan. It helps you prioritize your spending and control your expenses. Start by categorizing your expenses into essentials (such as housing, transportation, and groceries) and non-essentials (subscriptions, dining out, entertainment). Set realistic limits for each category and ensure that your total expenses are less than your income to achieve a positive cash flow.

4. Implementing smart saving strategies: Saving is an integral part of financial planning. Look for opportunities to save money on regular expenses, such as shopping for discounted items or using coupons. Consider setting up automatic transfers to a dedicated savings account, making it easier to save consistently. Additionally, explore investment options that align with your risk tolerance and long-term goals to grow your wealth over time.

5. Regularly reviewing and adjusting your plan: Financial planning is an ongoing process that requires periodic reviews and adjustments. Make it a habit to review your budget, track your progress, and make necessary tweaks to keep up with any changes in your financial situation or goals. Regularly monitoring your plan will ensure that it remains relevant and effective in helping you achieve financial success.

By following these strategies and tailoring them to your individual circumstances, you can create a budget that aligns with your financial aspirations and empowers you to make sound financial decisions. Start taking control of your finances today and set yourself up for a prosperous future!

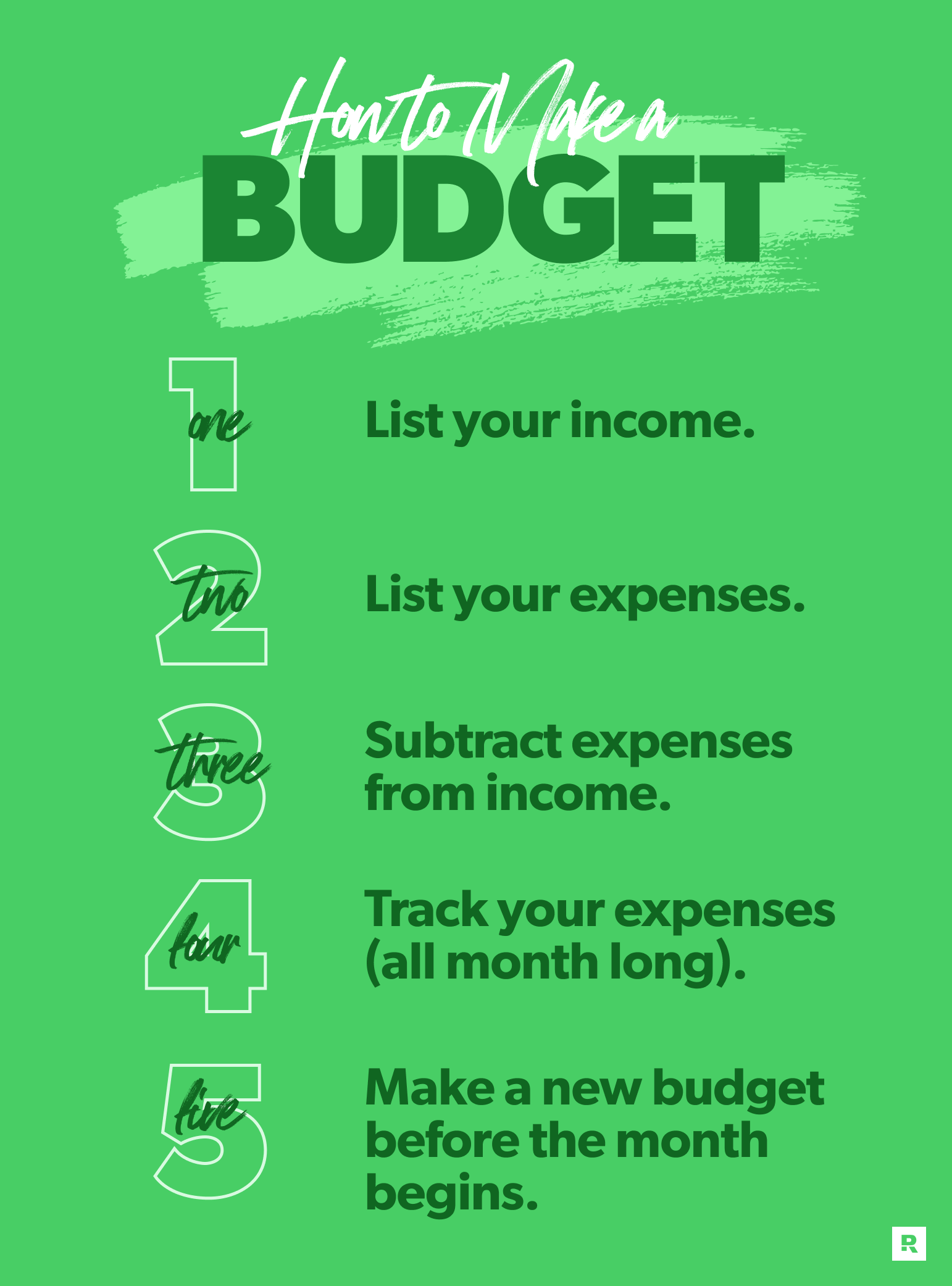

Step 1: Assess Your Financial Situation

Begin the process of creating a successful budget by carefully examining and evaluating your current financial position. This initial step is essential in gaining a clear understanding of your financial circumstances and setting a solid foundation for effective budgeting.

Take a comprehensive look at your income, expenses, and debt. Identify your sources of income and determine the exact amounts you receive regularly. Evaluate your expenses, both fixed and variable, and categorize them to gain insight into where your money is being spent.

It is important to also assess your existing debt, including loans, credit card balances, and any other outstanding payments. Taking stock of your debt will give you a realistic view of your financial obligations and help you make informed decisions on how to manage and reduce it.

During this assessment, consider your short-term and long-term financial goals. Whether it’s saving for a down payment, paying off a loan, or planning for retirement, defining your goals is crucial for creating a budget that aligns with your financial aspirations.

Finally, reflect on your spending habits and identify areas where you can make adjustments. This self-reflection will help you become aware of unnecessary expenses and provide opportunities to cut back on non-essential items.

Taking the time to assess your financial situation enables you to have a clear understanding of your income, expenses, debt, and goals. This in-depth evaluation will serve as a solid starting point as you continue to develop a budget that is tailored to your specific needs and objectives.

Gather all financial documents

In order to create a successful budget, it is essential to start by gathering all of your financial documents. These documents include records of your income, expenses, debts, and any other relevant financial information. By assembling these documents, you will have a comprehensive overview of your current financial situation, which is crucial for effective budgeting.

Begin by collecting your income-related documents, such as pay stubs, tax returns, and any other sources of income documentation. These documents will provide you with an accurate understanding of your monthly or annual income.

Next, gather all of your expense-related documents, including bills, bank statements, credit card statements, and receipts. Make sure to categorize your expenses into different sections, such as housing, transportation, utilities, food, entertainment, and others. This will enable you to clearly see where your money is going and identify any areas where you can potentially reduce expenses.

Additionally, it is important to gather information about your debts, such as loan agreements, credit card statements, and any other outstanding balances. Understanding the amount you owe and the associated interest rates will help you develop a plan to pay off your debts effectively.

Lastly, gather any other financial documents that may be relevant, such as investment statements, retirement account information, and savings account details. These documents will provide insight into your long-term financial goals and help you allocate funds accordingly.

By gathering all of these financial documents, you will have a complete picture of your financial situation. This will serve as a foundation for creating a budget that is tailored to your specific needs and goals, setting you on the path towards financial success.

Analyze your income and expenses

Understanding your financial situation is a vital step in creating an effective budget. By thoroughly analyzing your income and expenses, you can gain insight into your spending habits and make informed decisions about your financial goals.

Start by examining your income sources. This includes your salary or wages, freelance or side gig income, investment returns, and any other money that comes into your bank account. Consider the frequency and consistency of these income streams to get a clearer picture of how much money you can expect to have each month.

Next, take a close look at your expenses. Categorize them into fixed and variable expenses. Fixed expenses are those that stay constant each month, such as rent or mortgage payments, utility bills, and loan repayments. Variable expenses, on the other hand, fluctuate from month to month and may include groceries, entertainment, and transportation costs.

Once you have identified your income and expenses, it’s essential to compare them. Analyze how much you are earning versus how much you are spending. This will help you determine whether you have a surplus or a deficit. Understanding this balance is crucial for making adjustments to your budget and achieving your financial goals.

Consider using a table to organize your income and expenses. List each income source and expense category separately, along with the corresponding amounts. This visual representation will allow you to spot patterns, identify areas where you can potentially cut back or increase your income, and track your progress over time.

Remember, analyzing your income and expenses is an ongoing process. As your financial situation changes, it’s important to revisit and adjust your budget accordingly. Regularly monitoring and reassessing your income and expenses will help you stay on track and ensure that your budget continues to work effectively in achieving your financial goals.

| Income Sources | Amount |

|---|---|

| Salary | $3,500 |

| Freelance Income | $500 |

| Investment Returns | $200 |

| Total Income | $4,200 |

| Expenses | Amount |

|---|---|

| Rent | $1,200 |

| Utilities | $200 |

| Loan Repayments | $300 |

| Groceries | $400 |

| Entertainment | $150 |

| Transportation | $100 |

| Total Expenses | $2,350 |

Step 2: Set Clear Financial Goals

When embarking on your journey towards financial stability, it is crucial to set clear and achievable goals. These goals will serve as a guiding light, helping you make confident financial decisions and staying focused on your long-term plans.

The first step in setting clear financial goals is to identify what you truly value and desire in your life. Take a moment to reflect on your aspirations and dreams. Whether it’s purchasing a home, saving for your children’s education, or enjoying a comfortable retirement, understanding your priorities will enable you to align your budget with your goals.

Once you have a clear vision of your financial objectives, it’s time to break them down into smaller, manageable milestones. By breaking your goals into achievable steps, you can track your progress and stay motivated along the way. Consider setting both short-term and long-term goals to create a balanced and well-rounded financial plan.

Next, it’s essential to establish a timeline for each goal. Assigning specific timeframes will create a sense of urgency and help you stay on track. Be realistic when determining deadlines, considering factors such as your income, expenses, and savings capacity. Remember that Rome wasn’t built in a day, and it’s okay to adjust your timeline as necessary.

In addition to setting clear goals and timelines, it’s crucial to assign financial values to each objective. By assigning a monetary value to your goals, you can accurately assess how much you need to save or invest to achieve them. This will guide you in making informed decisions about your income allocation and expenditure choices.

Finally, regularly reassess and revise your financial goals as your circumstances and priorities may change over time. Life is dynamic, and it’s essential to adapt your goals to ensure they remain in line with your evolving needs and aspirations.

- Reflect on your aspirations and dreams

- Break goals into smaller, manageable milestones

- Establish a timeline for each goal

- Assign financial values to each objective

- Regularly reassess and revise your financial goals

By setting clear and meaningful financial goals, you embark on a path towards financial success and peace of mind. With a well-defined roadmap, you can confidently navigate the world of budgeting and ensure that your hard-earned money is working for you.

Identify short-term and long-term goals

In order to create a budget that truly works for you, it is crucial to identify both your short-term and long-term financial goals. These goals will serve as the guiding force behind your budgeting decisions and will help you prioritize your spending and saving.

Short-term goals

Short-term goals are the goals that you hope to achieve within the next year or so. They can include anything from saving up for a vacation or a down payment on a car, to paying off a credit card debt or an emergency fund. It is important to be specific when setting short-term goals, as this will help you accurately estimate the amount of money you need to allocate towards each goal. By identifying your short-term goals, you can create a budget that focuses on meeting these goals in a timely manner.

Long-term goals

Long-term goals are the goals that you hope to achieve in the distant future, typically beyond five years. These goals can include saving for retirement, buying a house, or funding your children’s education. While it may be harder to estimate the exact amount of money needed for long-term goals, it is still important to have a general idea of what you want to achieve. By identifying your long-term goals, you can start planning and saving accordingly, ensuring that you are on track to achieve them.

Identifying both short-term and long-term goals is a crucial step in creating a budget that aligns with your financial aspirations. By understanding what you want to achieve, you can make informed decisions about how to allocate your income and expenses, and have a clear roadmap towards financial success.

Make your goals specific, measurable, attainable, relevant, and time-bound (SMART)

- Specific: Start by defining your goals with clarity and precision. Instead of setting a vague goal like save money, be specific about how much money you want to save and for what purpose.

- Measurable: Make sure your goals are measurable so that you can track your progress. Use numbers or percentages to quantify what you want to achieve, such as saving a certain amount of money each month.

- Attainable: Set goals that are realistic and attainable within your current financial situation. Consider your income, expenses, and other financial obligations when determining what you can realistically achieve.

- Relevant: Align your goals with your overall financial objectives. Ensure that your goals are relevant to your financial aspirations and priorities, such as paying off debt, saving for a down payment, or building an emergency fund.

- Time-bound: Give your goals a deadline to create a sense of urgency and motivate yourself to take action. Set specific dates or timeframes for achieving each goal to hold yourself accountable.

By making your goals SMART, you can increase your chances of success and make your budgeting efforts more effective. Take the time to thoughtfully craft your goals, keeping in mind the principles of specificity, measurability, attainability, relevance, and time-bound nature. With SMART goals in place, you can take control of your finances and achieve your desired financial outcomes.

Step 3: Develop a Feasible Spending Plan

When it comes to managing your finances effectively, one crucial step is to create a realistic budget plan. Developing a feasible spending plan allows you to allocate your resources wisely and ensure that you can meet your financial goals.

A realistic budget plan involves assessing your income, expenses, and financial obligations. It requires careful consideration of your financial priorities and making smart decisions about how to allocate your money.

To create a realistic budget plan, start by taking an inventory of your income sources. This includes your salary, any additional sources of income, and even potential windfalls such as bonuses or tax refunds. It’s essential to have a clear understanding of how much money you have coming in regularly.

Next, evaluate your current expenses. Consider both fixed expenses, such as rent or mortgage payments, utilities, and insurance, as well as variable expenses like groceries, entertainment, and transportation costs. Take note of any debts or financial commitments that require regular payments.

Once you have a comprehensive picture of your income and expenses, it’s time to make decisions about how to distribute your funds. Prioritize essential expenses like housing, utilities, and debt payments. Then, allocate a portion of your income toward savings or investments to build financial security.

Keep in mind that a realistic budget plan involves finding a balance between spending and saving. It’s important to set aside some money for discretionary expenses like entertainment or dining out, while still ensuring that you are saving enough to meet your long-term financial goals.

- Assess your income sources and determine your total monthly income.

- Analyze your current expenses, including fixed and variable costs.

- Prioritize your essential expenses and allocate funds accordingly.

- Allocate a portion of your income towards savings or investments.

- Maintain a balance between spending and saving to achieve your financial goals.

By creating a realistic budget plan, you can gain control over your finances and make informed decisions about your spending. Remember that your budget is a flexible tool that can be adjusted as needed to accommodate changes in your financial situation or goals.

Track Your Income and Expenses

Monitoring your financial inflows and outflows is an essential step in effectively managing your money. By keeping a close eye on your income and expenses, you can gain a clear understanding of where your money is coming from and where it is going.

Keeping track of your income involves documenting all the different sources through which you receive money, including your salary, investments, side hustles, and any other additional income streams. By carefully recording these sources, you can have a comprehensive overview of your total earnings.

Similarly, tracking your expenses involves diligently noting down every expenditure you make, from fixed bills and essential purchases to discretionary spending. By categorizing your expenses into different groups like housing, transportation, groceries, entertainment, and others, you can get an accurate breakdown of your spending habits.

Tracking your income and expenses provides you with valuable insights into your financial patterns and habits. It allows you to identify areas where you may be overspending or ignoring potential sources of income. This knowledge can help you make informed decisions and adjustments to your budget as needed.

One effective way to track your income and expenses is by using a spreadsheet or a budgeting app. These tools enable you to easily input and analyze your financial data, providing you with visual representations of your income and expenses over time. With this information at hand, you can make proactive financial decisions and work towards achieving your financial goals.

To ensure accurate tracking of your income and expenses, it is important to establish a routine. Set aside regular time intervals, such as weekly or monthly, to review and update your financial records. By consistently monitoring your finances, you can maintain control over your budget and stay on top of your financial well-being.

Categorize your expenses and allocate a budget for each category

Organizing your expenses into different categories and setting a designated budget for each category is a crucial step in creating an effective budget. By categorizing your expenses, you can gain better visibility into your spending habits and make informed decisions about where to allocate your money.

Start by analyzing your past expenses and identifying common spending patterns. You can categorize your expenses into broad categories such as housing, transportation, groceries, discretionary spending, and debt payments. Within each category, further break down the expenses into more specific subcategories.

-

For example, under the housing category, you can include expenses such as rent/mortgage, utilities, insurance, and maintenance costs.

-

Under transportation, you can allocate a budget for expenses like fuel, car maintenance, public transportation costs, and parking fees.

-

The groceries category can include expenses for food, household supplies, and personal care items.

-

Discretionary spending can cover expenses related to entertainment, dining out, hobbies, and personal indulgences.

-

Lastly, debt payments category can include your monthly payments towards credit cards, loans, or any other outstanding debts.

Once you have categorized your expenses, it’s time to allocate a budget for each category. This involves determining how much you can afford to spend in each category and setting realistic limits to ensure you don’t overspend.

Consider your income, current financial obligations, and savings goals when allocating your budget. It’s important to strike a balance between different categories and prioritize essential expenses over discretionary ones. Allocating a specific amount to each category will help you track your spending and stay within your budget throughout the month.

Keep in mind that your budget allocation may need adjustments over time based on changes in your financial situation or goals. Regularly reviewing and adjusting your budget will ensure it remains effective and aligned with your needs.

By categorizing your expenses and assigning a budget for each category, you can gain better control over your finances and work towards your financial goals.

Consider including savings and emergency funds in your budget

When it comes to managing your finances effectively, it’s important to not only focus on your immediate expenses and financial goals, but also to plan ahead for unexpected circumstances and build a safety net. One way to achieve financial stability is by including savings and emergency funds in your budget.

While it may be tempting to allocate all your income towards current expenses and desires, neglecting to save for the future can leave you vulnerable to financial hardships. By setting aside a portion of your income for savings and emergency funds, you can ensure you have a cushion to fall back on in case of unexpected events such as medical emergencies, job loss, or major repairs.

When including savings and emergency funds in your budget, it’s essential to determine how much you can afford to save each month. Evaluate your income and expenses to identify areas where you can cut back and redirect those funds towards savings. It’s crucial to strike a balance between saving for the future and meeting your present needs.

Creating a separate savings account specifically for emergency funds can help you resist the temptation to dip into those funds for non-emergency expenses. Consider automating regular transfers from your primary account to your emergency fund to ensure consistent savings. Additionally, explore options such as high-interest savings accounts or investment vehicles that can help your savings grow over time.

Having savings and emergency funds in your budget not only provides a sense of security but also allows you to pursue your financial goals without the constant worry of unexpected expenses. It gives you the freedom to make choices that align with your long-term plans and aspirations.

In summary, don’t overlook the importance of including savings and emergency funds in your budget. This strategic approach to managing your finances can help you weather financial storms and build a solid foundation for a secure future.

Step 4: Implement and Monitor Your Spending Plan

Now that you have successfully outlined and organized your financial goals, income, and expenses, it is time to put your budget into action. Implementation and monitoring are crucial steps in ensuring the effectiveness of your spending plan. By consistently tracking your spending and comparing it to your budgeted amounts, you will be able to identify any deviations and make necessary adjustments to stay on track.

One effective way to implement and monitor your budget is by creating a table that lists your budgeted amounts for each expense category alongside the actual amounts you spend. This allows you to easily compare your planned budget with your actual spending and assess if you are adhering to your financial goals. Regularly reviewing this table will provide you with insight into your spending patterns and enable you to make informed decisions about where adjustments need to be made.

In addition to tracking your expenses, it is essential to monitor your income as well. Keep a record of all your income sources, such as your salary, freelance work, or side businesses. Compare your actual income to your projected income to ensure that you are meeting your financial targets and making progress towards your goals.

Monitoring your budget also involves being mindful of any unexpected or irregular expenses that may arise. These could include medical bills, car repairs, or home maintenance. By setting aside funds in your budget for such unpredictable expenses, you will be better prepared and less likely to disrupt your overall financial plan.

Consistency is key when it comes to implementing and monitoring your budget. Make it a habit to regularly review and update your spending plan. Consider using budgeting tools or apps to simplify the process and automate tracking. By staying diligent and committed to your budget, you are setting yourself up for financial success and taking control of your financial future.

| Expense Category | Budgeted Amount | Actual Amount |

|---|---|---|

| Housing | $1,200 | $1,100 |

| Transportation | $300 | $350 |

| Groceries | $200 | $180 |

| Entertainment | $100 | $120 |

| Debt Payments | $500 | $550 |

Questions and answers

What is the first step to creating a budget?

The first step to creating a budget is to track your income and expenses. This helps you understand where your money is coming from and where it is going.

How can budgeting help improve my financial situation?

Budgeting can help improve your financial situation by allowing you to see where you are spending money unnecessarily and where you can cut back. It helps you prioritize your expenses and save more effectively.

Should I include savings in my budget?

Yes, it is important to include savings in your budget. Allocating a portion of your income towards savings ensures that you have a financial safety net and can cover unexpected expenses.

What should I do if my expenses exceed my income?

If your expenses exceed your income, it is necessary to reevaluate your spending habits. Look for areas where you can cut back and make adjustments to your budget accordingly. It may also be helpful to explore options for increasing your income, such as taking on a part-time job or freelancing.

How often should I review and adjust my budget?

It is recommended to review and adjust your budget on a monthly basis. This allows you to track your progress, identify any changes in your financial situation, and make necessary adjustments to ensure your budget remains effective.

Why is creating a budget important?

Creating a budget is important because it allows you to track and control your expenses, effectively manage your money, and achieve financial goals.

How can I track my expenses?

You can track your expenses by recording them in a notebook, using a spreadsheet, or by using budgeting apps and tools available online. Choose a method that suits your preferences and makes it easy for you to track your expenses.

How often should I review and adjust my budget?

It is recommended to review and adjust your budget monthly or whenever there are significant changes in your income or expenses. This will help ensure that your budget remains realistic and effective.