Have you ever wondered what it takes to gain complete control over your finances and attain a state of true financial freedom? Many individuals strive to achieve this sought-after milestone, seeking ways to manage their money wisely and make it work for them. In this article, we will explore the essential steps that can help you pave the way towards financial independence using intelligent financial strategies.

First and foremost, it is crucial to underscore the significance of understanding your financial goals and aspirations. Whether you aspire to retire early, start your dream business, or travel the world, having a clear vision of what you want to achieve is paramount in this journey. By identifying your financial objectives, you can tailor your money management decisions to support these ambitions and set yourself up for success.

Revolutionize Your Health & Lifestyle!

Dive into the world of Ketogenic Diet. Learn how to lose weight effectively while enjoying your meals. It's not just a diet; it's a lifestyle change.

Learn MoreNext, it is imperative to develop a comprehensive understanding of your current financial situation. This involves a meticulous assessment of your income, expenses, assets, and liabilities. By honestly evaluating your financial standing, you can identify areas of improvement and devise a plan that emphasizes strategic money allocation and eliminating unnecessary expenditures. This self-awareness is essential for creating a strong foundation on which you can build your path to financial independence.

Once armed with a clear vision and a solid understanding of your financial landscape, it’s time to strategically plan and prioritize. Creating a budget that aligns with your goals allows you to allocate your income in a way that maximizes savings and minimizes unnecessary spending. By evaluating your expenses and finding areas to cut back, you can redirect those funds towards investments or savings accounts that will yield long-term benefits. Additionally, it’s important to start an emergency fund to secure your financial stability in case unexpected expenses arise.

- Understanding Financial Freedom

- What is Financial Independence?

- Definition and Importance

- Creating a Budget

- Evaluating Income and Expenses

- Calculating Monthly Cash Flow

- Identifying Areas for Cost Reduction

- Debt Reduction and Savings

- Paying off High-Interest Debts

- Strategies for Accelerated Debt Repayment

- Building an Emergency Fund

- Investing for the Future

- Understanding Different Investment Options

- Questions and answers

Understanding Financial Freedom

In the pursuit of true financial independence, it is crucial to grasp the concept and significance of financial freedom. This section aims to provide an insightful exploration of what financial freedom entails, without explicitly using the terms steps, achieve, financial, independence, through, smart, money, and management.

Financial liberation implies attaining a state of economic autonomy, where individuals possess the ability to make choices and dictate their financial destinies. A core principle underlying financial liberation is the aptitude to create and sustain wealth, free from constraints or reliance on external sources. By understanding the art of managing personal finances wisely and establishing sound financial habits, one can gradually break free from financial limitations and embark on a path towards liberation.

Obtaining financial independence necessitates exercising prudence and discipline when it comes to utilization of financial resources. Cultivating a deep-rooted understanding of personal finances, including budgeting, saving, and investing, empowers individuals to control their current and future financial situations. By identifying and differentiating between needs and wants, and by prioritizing long-term goals over short-term gratification, one can proactively build a solid financial foundation.

Moreover, gaining financial freedom involves developing a mindset focused on building wealth and creating multiple income streams. This involves cultivating entrepreneurial skills and seeking opportunities for growth and diversification. By exploring various investment avenues and adapting to ever-changing financial landscapes, individuals can optimize their financial potential and ultimately break free from the shackles of financial dependence.

It is important to note that financial independence is not solely measured by the size of one’s bank account, but rather by the sense of security and peace of mind that comes with having control over one’s financial future. Understanding the fundamental principles and strategies for achieving financial freedom serves as a compass on this transformative journey, paving the way for sustainable wealth creation and a fulfilling life.

What is Financial Independence?

Financial independence is the state of being able to comfortably support oneself without relying on external sources of income. It involves managing resources efficiently in order to achieve a sustainable and secure financial position.

|

Self-sufficiency |

Achieving financial independence means being self-sufficient in terms of income and expenses. It is about having the means to cover daily living expenses, unexpected emergencies, and future financial goals without depending on others. |

|

Freedom of choice |

Financial independence provides individuals with the freedom to make choices based on their values and goals rather than financial constraints. It allows them to pursue their passions, take risks, and follow a path that aligns with their true aspirations. |

|

Peace of mind |

Attaining financial independence brings a sense of security and peace of mind. Knowing that one has the financial resources to handle unexpected circumstances and retire comfortably provides a strong sense of stability and reduces stress. |

In summary, financial independence is the ability to support oneself and make choices without being constrained by financial limitations. It provides self-sufficiency, freedom of choice, and peace of mind, ultimately leading to a more fulfilling and secure lifestyle.

Definition and Importance

In the realm of personal finance, understanding the concept of financial independence and its significance is crucial for individuals seeking to gain control over their financial lives. Financial independence can be defined as the state of being self-reliant and self-sufficient in terms of managing one’s own finances. It is a state where individuals have enough financial resources to support their desired lifestyle and meet their financial goals without relying on others or being burdened by debt. Attaining financial independence is not only essential for personal well-being but also provides a sense of security, freedom, and flexibility in making financial decisions.

Recognizing the importance of financial independence empowers individuals to take proactive steps towards effective money management, prudent spending, and strategic investment. It enables individuals to break free from the cycle of living paycheck to paycheck, accumulating debt, or relying on others for financial support. Financial independence gives individuals the ability to pursue their passions, dreams, and long-term aspirations without financial constraints. It offers the opportunity to create a solid foundation for future financial stability, allowing individuals to weather unexpected expenses, emergencies, or economic downturns.

Gaining financial independence requires a comprehensive understanding of personal finance principles, including budgeting, saving, investing, and debt management. It entails setting realistic financial goals, living within one’s means, and making conscious decisions about spending and saving. Achieving financial independence may involve careful planning, discipline, and perseverance. However, the rewards of financial independence are immeasurable, providing individuals with a sense of empowerment, peace of mind, and the ability to enjoy the fruits of their labor while building a secure financial future.

- Understanding the concept of financial independence and its importance for personal financial well-being.

- The significance of being self-reliant and self-sufficient in managing one’s own finances.

- Breaking free from the cycle of debt and living paycheck to paycheck.

- Creating a solid foundation for future financial stability.

- Empowering individuals to pursue their passions and aspirations without financial constraints.

- Comprehensive understanding of personal finance principles.

- Setting realistic financial goals and making conscious decisions about spending and saving.

- The rewards of financial independence.

Creating a Budget

Building a financial strategy that helps you take control of your money and work towards your financial goals starts with creating a budget. This crucial step allows you to carefully examine your income, expenses, and spending habits, ensuring you make informed decisions about your finances.

Budgeting is the foundation for effective money management. It involves carefully tracking and categorizing your income and expenditures, giving you a clear picture of where your money is coming from and where it is going. By establishing a budget, you can prioritize your spending, cut unnecessary expenses, and redirect your funds towards meaningful financial pursuits.

Crafting a budget empowers you to make intentional choices about how you allocate your resources, enabling you to work towards long-term financial stability and independence. It allows you to understand your financial position, identify areas for improvement, and lay the groundwork for successful wealth creation.

When creating a budget, start by evaluating your income. This includes not only your primary source of income, such as your salary, but also any additional income streams, such as rental properties or freelance work. Understanding your total monthly income is essential for accurate budgeting.

Next, analyze your expenses. Categorize your expenses into fixed costs, such as rent or mortgage payments, utilities, and insurance, and variable costs, including groceries, entertainment, and travel. This breakdown allows you to identify areas where you can potentially reduce spending and increase savings.

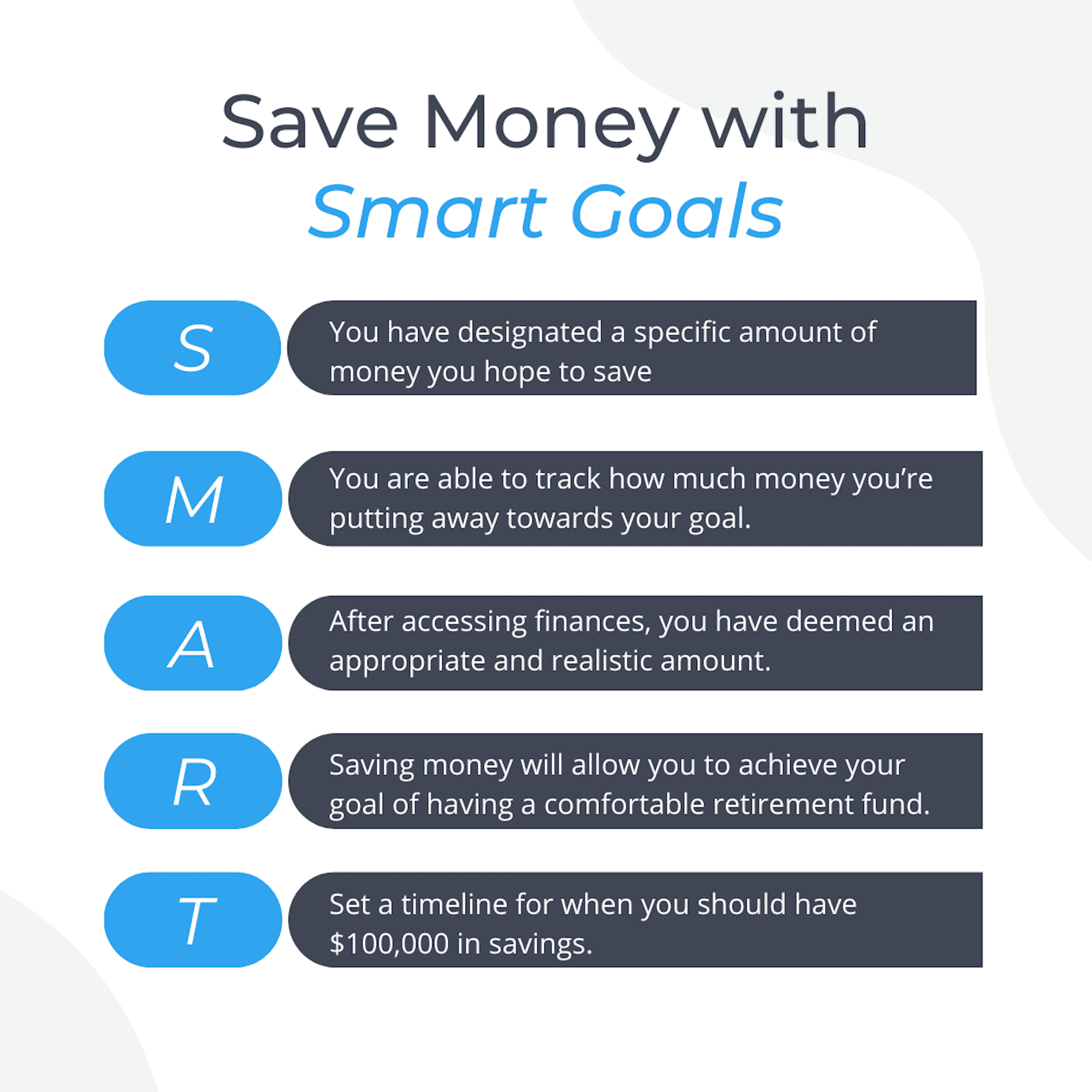

Once you have a clear picture of your income and expenses, set financial goals. Whether it’s saving for a down payment on a house, starting a retirement fund, or paying off debt, defining clear and realistic objectives helps guide your budgeting decisions, ensuring your spending aligns with your long-term financial aspirations.

Remember, creating a budget is an ongoing process. Regularly review and revise your budget to reflect changes in your income and expenses. Stay committed to your budgeting goals, monitoring your progress against them, and making adjustments as necessary to stay on track towards achieving financial independence.

Evaluating Income and Expenses

In this section, we will explore the process of assessing your earnings and expenditures to gain a deeper understanding of your financial situation. By thoroughly examining your sources of income and evaluating your expenses, you can make informed decisions to optimize your financial well-being.

Analyzing Income:

Evaluating your income involves assessing all the different streams of money that flow into your life, whether it is from employment, investments, or other sources. Take into account not only your regular paycheck but also any bonuses, overtime, or side income. By understanding the total amount and nature of your income, you can better plan your financial goals and budget accordingly.

Assessing Expenses:

Once you have a clear picture of your income, it’s important to evaluate your expenses. This includes categorizing and tracking your spending, ensuring that you have insight into where your money is going. Analyze your fixed expenses, such as rent or mortgage payments, utility bills, and loan repayments, as well as variable costs like groceries, entertainment, and discretionary spending. Identifying areas where you can reduce expenses or eliminate unnecessary expenditures can significantly impact your financial independence journey.

Identifying Financial Priorities:

After evaluating your income and expenses, it’s crucial to prioritize your financial goals. Determine what matters most to you in terms of short-term and long-term objectives. This could include building an emergency fund, paying off debt, saving for retirement, or investing in assets. By identifying your financial priorities, you can allocate your resources effectively and work towards achieving them.

Creating a Budget:

Based on your income, expenses, and financial priorities, it is important to create a budget that aligns with your goals. A budget acts as a roadmap for managing your money and ensures that you are spending within your means. Allocate funds for essential expenses, savings, and investments while allowing for some flexibility for discretionary spending. Regularly review and adjust your budget as your financial circumstances change.

Tracking Progress:

Finally, regularly track and monitor your income and expenses to measure your progress towards financial independence. This involves reviewing your budget, tracking your spending, and comparing it to your goals. By periodically evaluating your financial situation, you can make necessary adjustments and stay on track towards achieving your desired level of financial independence.

Remember, thoroughly evaluating your income and expenses is a crucial step in achieving financial independence. By gaining a clear understanding of your financial situation, you can make informed decisions and take control of your financial future.

Calculating Monthly Cash Flow

Understanding your monthly cash flow is crucial for achieving financial independence.

When it comes to managing your finances wisely and working towards financial independence, one of the most important steps is calculating your monthly cash flow. Your monthly cash flow represents the amount of money coming in and going out of your bank account each month, and it serves as the foundation for your financial planning.

To calculate your monthly cash flow, you need to consider all sources of income and expenses. This includes your salary or wages, any additional income from investments or side hustles, and any other sources of income you may have. On the expense side, you need to account for all your regular bills, such as rent or mortgage payments, utilities, groceries, transportation costs, and any other monthly expenses.

Once you have a comprehensive list of your income and expenses, you can calculate your monthly cash flow by subtracting your total expenses from your total income. If your income exceeds your expenses, you have a positive cash flow, which means you have money left over each month that you can allocate towards savings or investments. On the other hand, if your expenses surpass your income, you have a negative cash flow, which indicates that you are living beyond your means and need to reevaluate your spending habits and make adjustments to balance your budget.

Knowing your monthly cash flow is essential for making informed financial decisions. It allows you to identify areas where you can cut back on expenses or find ways to increase your income. By analyzing your cash flow, you can create a realistic budget, set financial goals, and track your progress towards financial independence.

In conclusion, calculating your monthly cash flow is a crucial step in smart money management that can help you achieve financial independence. It provides a clear picture of your financial situation and empowers you to make informed decisions about your spending and saving habits.

Identifying Areas for Cost Reduction

In order to attain financial freedom and gain control over your finances, it is crucial to identify areas in your life where cost reduction can be implemented. By examining and evaluating various aspects of your spending habits, you can uncover opportunities to reduce expenses and maximise your savings. This section aims to guide you through the process of identifying these areas and taking necessary steps towards achieving your financial goals.

One effective method for identifying areas for cost reduction is conducting a thorough analysis of your monthly budget. By closely examining your expenses, you can identify recurring costs and assess their necessity and value. Consider categorizing your expenses into different segments, such as housing, transportation, food, entertainment, and utilities. This will allow you to identify which areas consume a significant portion of your income and where potential savings can be made.

| Expense Category | Monthly Expenditure | Potential Cost Reduction |

|---|---|---|

| Housing | $1500 | Exploring cheaper rental options or refinancing a mortgage |

| Transportation | $500 | Using public transportation or carpooling instead of owning a vehicle |

| Food | $400 | Meal planning, cooking at home, and reducing dining out expenses |

| Entertainment | $200 | Exploring free or lower-cost entertainment options, such as community events or streaming services |

| Utilities | $250 | Conserving energy, switching to more energy-efficient appliances, and comparing utility providers for better rates |

Another aspect to consider is the comparison of prices and services for recurring bills, such as insurance, mobile phone plans, and internet providers. Researching and comparing different options can often lead to discovering better deals or negotiating lower rates, potentially resulting in significant savings over time.

In addition, it is important to assess your discretionary spending habits. While it is essential to allocate a portion of your budget for leisure and personal enjoyment, it is equally important to ensure that these expenses are aligned with your financial goals. Look for opportunities to reduce unnecessary expenses, such as cutting back on impulse purchases or finding creative alternatives that offer similar enjoyment at a lower cost.

Identifying areas for cost reduction requires discipline, patience, and a willingness to make changes in your spending habits. Remember, every small adjustment can add up to significant savings over time, contributing to your journey towards financial independence.

Debt Reduction and Savings

In this section, we will focus on two crucial aspects of achieving financial independence: reducing debt and cultivating savings. These strategies are essential for individuals looking to improve their financial situation and gain control over their money.

One of the key steps towards financial independence is decreasing and managing debt effectively. By proactively addressing outstanding debts, individuals can alleviate financial burdens and improve their overall financial health. It is important to create a structured plan to pay off debts, prioritizing high-interest loans first to minimize the total amount paid over time. Additionally, adopting responsible borrowing habits and avoiding unnecessary debts can prevent further financial strain.

Another critical element in achieving financial independence involves developing a habit of saving regularly. Setting aside a portion of your income each month can provide a safety net for unexpected expenses and future investments. Building an emergency fund is crucial to avoid relying on credit cards or loans during unforeseen circumstances. By consistently saving, individuals can contribute towards long-term goals such as retirement, education, or purchasing assets.

When managing debt and savings simultaneously, it is important to strike a balance between the two. While it is crucial to pay off high-interest debts promptly, neglecting savings entirely can leave individuals vulnerable to future financial challenges. Prioritizing debt reduction and savings concurrently can help individuals achieve a stable financial foundation and pave the way towards long-term financial independence.

Paying off High-Interest Debts

Eliminating debts with high interest rates is a crucial step towards achieving financial freedom. By prioritizing the repayment of these debts, individuals can effectively reduce the burden of interest expenses and regain control over their finances.

One of the key strategies in paying off high-interest debts is to develop a structured repayment plan. This entails assessing the outstanding balances, interest rates, and minimum payment requirements of each debt. By understanding the specific terms of these debts, individuals can allocate their resources wisely and focus on paying off the highest interest debts first.

Another approach to tackle high-interest debts is through debt consolidation or refinancing. This involves combining multiple debts into a single loan with a lower interest rate. By consolidating debts, individuals can simplify their repayment process and potentially reduce the overall interest paid over time.

Furthermore, it is important to explore opportunities for negotiating with creditors. By contacting lenders and demonstrating a commitment to repay the debt, individuals may be able to negotiate lower interest rates or establish more favorable repayment terms. This can help alleviate the financial strain and accelerate the debt payoff process.

In addition, it is crucial to consistently review and adjust the repayment plan as financial circumstances change. Regularly monitoring progress, reassessing priorities, and making necessary adjustments will ensure that individuals stay on track towards eliminating high-interest debts.

Paying off high-interest debts requires discipline, persistence, and a strategic approach. By implementing these strategies and maintaining a proactive mindset, individuals can achieve financial freedom and pave the way for long-term financial stability.

Strategies for Accelerated Debt Repayment

In this section, we will explore various approaches and techniques to expedite the process of paying off debts. By implementing these strategies, you can effectively reduce your debt burden and move closer to achieving your financial goals.

1. Rapid Repayment: One of the most effective ways to accelerate debt repayment is by increasing the amount of money you allocate towards paying off your debts each month. By prioritizing your debt payments and making consistent and substantial contributions, you can expedite the process and reduce the overall interest paid.

2. Debt Snowball: Another approach that can be highly effective is the debt snowball method. This strategy involves prioritizing your debts from smallest to largest and systematically paying them off one by one. As each debt is paid off, the freed-up funds can then be applied towards the next debt, creating a snowball effect that gains momentum over time.

3. Debt Consolidation: For individuals with multiple debts from different sources, consolidating them into a single loan or credit card can simplify the repayment process and potentially lower interest rates. By merging your debts, you can streamline payments and potentially reduce the overall amount of interest paid.

4. Negotiating Lower Interest Rates: It’s worth exploring the option of negotiating lower interest rates with your lenders. By demonstrating a strong repayment plan and a commitment to paying off your debts, some lenders may be willing to lower your interest rates, which can significantly reduce the total amount paid over time.

5. Seeking Professional Help: If you find yourself overwhelmed by debt or struggling to develop a repayment plan, seeking professional assistance from a financial advisor or credit counseling service can provide valuable guidance. These experts can help you create a personalized repayment plan and negotiate with creditors on your behalf.

By implementing these strategies for accelerated debt repayment, you can take control of your financial situation and pave the way towards a debt-free future.

Building an Emergency Fund

In this section, we will explore the importance of creating a safety net for unexpected financial challenges. The focus will be on establishing an emergency fund.

Financial stability is crucial for leading a secure and stress-free life. However, unforeseen circumstances such as medical emergencies or job loss can quickly disrupt our financial balance. This is where an emergency fund becomes indispensable. It serves as a cushion to protect us during tough times, allowing us to weather the storm without resorting to debt or compromising our long-term financial goals.

An emergency fund provides a sense of security, knowing that there is money readily available to handle urgent situations. It allows individuals to avoid unnecessary stress or panic when faced with unexpected expenses. Whether it’s a car repair, medical bill, or sudden unemployment, having an emergency fund can make a significant difference in preserving our financial well-being.

Building an emergency fund requires discipline and consistent effort. It begins by setting a realistic savings goal, aiming for a financial safety net that covers at least three to six months’ worth of living expenses. While this may seem challenging at first, it is essential to start small and gradually increase the savings over time.

One effective strategy is to allocate a fixed percentage of your income towards the emergency fund every month. This systematic approach ensures that savings grow steadily without adversely affecting your day-to-day expenses. Consider automating the process by setting up automatic transfers from your primary bank account to a separate savings account designated for emergencies.

Another option is to cut back on non-essential expenses and redirect the savings towards your emergency fund. Review your monthly budget closely and identify areas where you can trim unnecessary spending. This could involve making small lifestyle adjustments such as reducing dining out, entertainment expenses, or finding cost-effective alternatives for various services.

A diverse range of income sources can also contribute to building an emergency fund. Exploring part-time jobs, freelancing opportunities, or passive income streams can increase your overall income and provide a more substantial base for your savings.

Finally, it’s crucial to resist the temptation to dip into the emergency fund for non-essential expenses. Remember that the primary purpose of this fund is to provide financial security during unforeseen circumstances. Maintain discipline and prioritize the longevity of your emergency fund for true peace of mind.

By proactively building an emergency fund, individuals can achieve a greater level of financial resilience and reduce the impact of unexpected events on their overall financial well-being.

Investing for the Future

Planning for a secure and prosperous future involves making strategic decisions about how to invest our money wisely. By allocating our resources intelligently and nurturing our financial assets, we can build a foundation for long-term growth and stability. In this section, we will explore the various avenues available for investing and discuss the key considerations to keep in mind while making investment decisions.

| Types of Investments | Expected Returns | Risk Level |

|---|---|---|

| Stocks | Potentially high | High risk |

| Bonds | Moderate | Medium risk |

| Real Estate | Varies | Medium to high risk |

| Mutual Funds | Varies | Medium risk |

| Exchange-Traded Funds (ETFs) | Varies | Medium risk |

| Cryptocurrencies | Highly volatile | High risk |

Each type of investment offers its own set of potential benefits and risks. Stocks, for example, provide the opportunity for high returns but also carry a higher level of risk. Bonds, on the other hand, offer more stable returns with moderate risk. Real estate investments can vary in terms of returns and risk depending on factors such as market conditions. Mutual funds and ETFs provide diversification and professional management, spreading the risk across a portfolio of assets. Cryptocurrencies, while potentially lucrative, are highly volatile and carry a significant level of risk.

When considering where to invest, it is essential to evaluate our risk tolerance, investment goals, and time horizon. Diversifying our investment portfolio across different asset classes can help mitigate risk and maximize potential returns. Regularly reviewing and rebalancing our investments ensures that they align with our changing financial circumstances and objectives.

In conclusion, investing for the future requires a thoughtful approach and informed decision-making. By understanding the different types of investments and their associated risks and returns, we can make strategic choices that will help us achieve our long-term financial goals.

Understanding Different Investment Options

Exploring various pathways to financial freedom necessitates a comprehensive understanding of the diverse investment options available. Acquiring knowledge of these options enables individuals to make informed decisions about where to allocate their funds. By comprehending the distinct characteristics, risks, and potential returns associated with different investment vehicles, individuals can tailor their investment strategies to meet their financial goals and aspirations.

- Stocks: Investing in stocks involves purchasing ownership shares in publicly traded companies. This investment option has the potential for high returns but is accompanied by a commensurate level of risk.

- Bonds: Bonds involve lending money to governments or corporations for a fixed period. They offer a predictable income stream and are typically considered less risky than stocks.

- Mutual Funds: Mutual funds pool money from multiple investors to invest in a diversified portfolio of securities. This option allows individuals to access professional management and diversification benefits.

- Real Estate: Real estate investments involve purchasing properties, such as residential homes, commercial buildings, or land, with the expectation of generating income or capital appreciation over time.

- Commodities: Investing in commodities entails purchasing physical goods, such as gold, oil, or agricultural products. This alternative investment can provide a hedge against inflation and diversification benefits.

- Exchange-Traded Funds (ETFs): ETFs are similar to mutual funds but trade on stock exchanges. They offer diversification, flexibility, and lower expenses compared to traditional mutual funds.

By understanding the characteristics, risks, and potential returns associated with these diverse investment options, individuals can create a well-rounded investment portfolio that aligns with their risk tolerance, time horizon, and financial objectives. It is essential to conduct thorough research, seek professional advice, and constantly monitor and adjust the portfolio to maximize investment success and achieve long-term financial independence.

Questions and answers

What are the steps to achieve financial independence?

The steps to achieve financial independence include creating a budget, controlling spending habits, investing wisely, building multiple streams of income, and consistently saving and planning for the future.

How can I create a budget to manage my finances?

To create a budget, start by listing all your monthly income and expenses. Categorize your expenses into fixed (rent, utilities) and variable (food, entertainment). Analyze your spending patterns and identify areas where you can cut back. Allocate a portion of your income towards savings and debt repayment. Regularly track your expenses and make adjustments accordingly.

What is the importance of controlling spending habits?

Controlling spending habits is crucial for achieving financial independence as it helps you avoid unnecessary debt and build savings. By distinguishing needs from wants, setting spending limits, and practicing restraint, you can make better financial decisions and prioritize long-term goals over short-term gratification.

How can I build multiple streams of income?

To build multiple streams of income, you can explore part-time jobs, freelancing, starting a side business, or investing in dividend-paying stocks or rental properties. Diversifying your income sources not only increases your earning potential but also helps safeguard against potential financial setbacks.

Why is it important to save consistently for the future?

Consistent saving for the future is important because it allows you to create an emergency fund, invest for retirement, and achieve your long-term financial goals. Saving regularly ensures that you have a financial cushion to fall back on during unexpected events and helps you secure your financial independence in the long run.

What is financial independence and why is it important?

Financial independence refers to the ability to sustain one’s lifestyle without relying on others for financial support. It is important because it provides individuals with freedom, choices, and peace of mind. It allows them to pursue their goals and dreams without the constraints of financial limitations.

What are some key steps to achieve financial independence?

Some key steps to achieve financial independence include creating a budget and tracking expenses, saving and investing wisely, reducing debt, increasing income through multiple sources, and setting financial goals. These steps help individuals in managing their money effectively and building wealth over time.

How can I create a budget and track my expenses?

To create a budget, start by listing your monthly income and fixed expenses. Then allocate funds for variable expenses such as groceries, entertainment, and transportation. Tracking expenses can be done through various methods such as using budgeting apps, spreadsheet software, or simply keeping receipts and recording them manually. Regularly reviewing and adjusting your budget is also crucial for effective money management.

What are some strategies to reduce debt?

Strategies to reduce debt include creating a debt payoff plan by prioritizing high-interest debts, negotiating lower interest rates, consolidating debts, and making extra payments whenever possible. It is also important to avoid accumulating new debt and to seek professional assistance, such as credit counseling, if necessary.

How can I increase my income through multiple sources?

To increase income through multiple sources, individuals can consider options such as starting a side business or freelancing, investing in real estate or stocks, monetizing hobbies or skills, or taking advantage of the gig economy. Diversifying income streams provides security and the potential for higher earnings.