In our fast-paced and uncertain world, it is crucial to acknowledge the weight of establishing a buffer for unforeseen circumstances. Having a secure financial foundation sets the stage for building a prosperous future, by mitigating potential hardships and offering a sense of peace and tranquility. By cultivating an adequate emergency fund, individuals can safeguard themselves against unexpected mishaps, bolster their financial resilience, and foster a greater sense of self-sufficiency.

Embracing the concept of fiscal preparedness, while seemingly abstract, is an essential element in navigating life’s uncertainties. As we embark on the journey of financial security, it becomes paramount to recognize the significance of amassing emergency savings. These funds serve as a financial lifeline during difficult times, acting as a panacea for sudden medical emergencies, job loss, unexpected home repairs, or any other unforeseen crises that may arise along life’s trajectory.

Revolutionize Your Health & Lifestyle!

Dive into the world of Ketogenic Diet. Learn how to lose weight effectively while enjoying your meals. It's not just a diet; it's a lifestyle change.

Learn MoreThe inception of a savings endeavor can often be perceived as a daunting task, but with a well-crafted plan in place, this endeavor can be both manageable and rewarding. By adopting prudent money management practices and cultivating daily savings habits, individuals can embark on a transformative journey towards long-term financial stability and freedom. This article serves as a comprehensive guide, offering valuable insights and step-by-step instructions to aid in the establishment of an effective emergency fund.

- The Significance of Emergency Savings: A Step-by-Step Guide

- Understanding the Significance

- Why Everyone Should Have Emergency Savings

- Financial Security in Unforeseen Circumstances

- Getting Started with Building your Emergency Fund

- Assessing Your Current Financial Situation

- Setting Realistic Saving Goals

- Assessing Your Financial Situation

- Prioritizing Your Saving Objectives

- Setting SMART Saving Goals

- Tracking and Adjusting Your Progress

- Creating a Dedicated Emergency Fund

- Building Your Emergency Savings

- Establishing a Budget and Cutting Expenses

- Automating Your Savings Contributions

- Exploring Supplemental Income Opportunities

- Maintaining and Utilizing Your Emergency Fund

- Questions and answers

The Significance of Emergency Savings: A Step-by-Step Guide

In today’s unpredictable world, having a safety net to fall back on during unforeseen circumstances is of great importance. Establishing a fund specifically dedicated to emergencies is a prudent step towards financial security. In this comprehensive guide, we will walk you through the significance of emergency savings and provide you with a step-by-step approach to building and maintaining yours.

Understanding the Value of Emergency Savings

Unexpected events such as job loss, medical emergencies, and major car repairs can drastically impact your financial stability. Having a dedicated emergency fund can offer peace of mind and a sense of security during these challenging times. By setting aside funds specifically for emergencies, you are better prepared to handle unexpected expenses without relying on credit cards or loans, which can lead to long-term debt.

The Step-by-Step Approach

Building emergency savings requires careful planning and consistent efforts. The step-by-step approach outlined below will guide you through the process:

- Evaluating Your Current Financial Situation: Start by assessing your income, expenses, and debt. Understanding your financial standing will help you determine how much you can feasibly save each month.

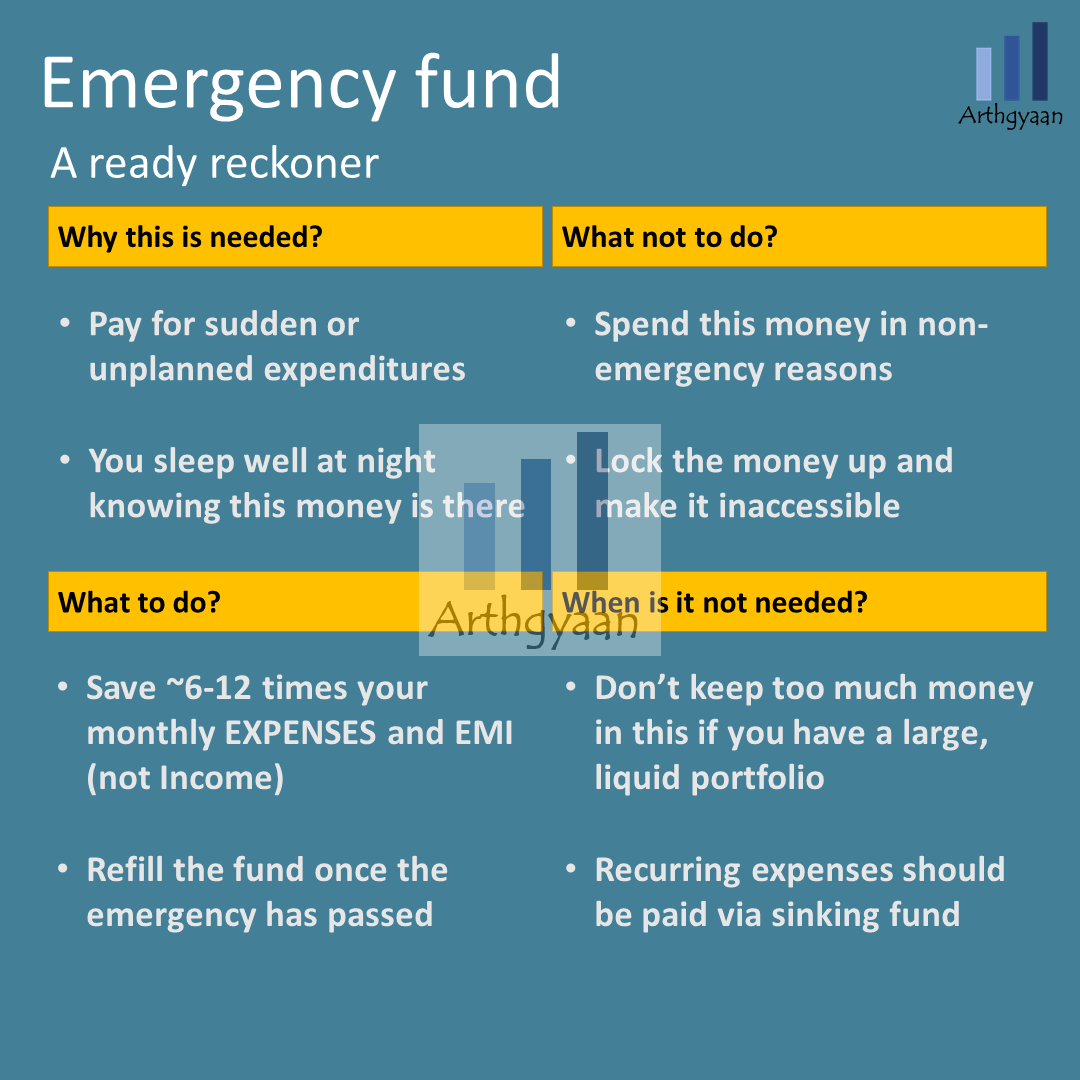

- Setting Realistic Savings Goals: Define a target amount for your emergency fund based on your monthly expenses and the recommended emergency savings guidelines. Aim to build a fund that covers at least six months’ worth of essential expenses.

- Creating a Budget: Develop a budget that prioritizes savings and allows you to allocate a portion of your income towards emergency savings. Cut back on non-essential expenses and redirect those funds to your savings account.

- Automating Savings: Set up automatic transfers from your checking account to your emergency fund on a regular basis. Automating your savings ensures consistency and reduces the temptation to spend the funds elsewhere.

- Building Emergency Savings Gradually: It’s important to start small if you are unable to save a significant amount initially. Consistency is key, so consistently contribute to your emergency fund even if the amounts are smaller.

- Seeking Additional Income Sources: Consider finding ways to increase your income through part-time work or freelancing. The extra income can be directly added to your emergency savings, accelerating your progress.

- Maintaining and Protecting Your Emergency Fund: Once you have built your emergency savings, it’s crucial to maintain it and refrain from using the funds for non-emergency purposes. Regularly review and adjust your savings plan as your financial situation evolves.

In conclusion, the significance of having emergency savings cannot be overstated. By following the step-by-step guide outlined above, you can confidently establish and maintain a fund that offers financial security and peace of mind during unexpected situations.

Understanding the Significance

In today’s fast-paced and uncertain world, it is crucial for individuals to realize the immense value of building a financial safety net. Acknowledging the relevance of having funds set aside in case of unexpected circumstances or emergencies is a fundamental step towards securing one’s financial well-being.

By comprehending the significance of establishing an emergency savings cushion, individuals can proactively protect themselves against unforeseen events and financial hardships that may arise. Having a firm grasp of this importance serves as a foundation for taking the necessary steps towards financial stability and peace of mind.

Recognizing the essence of emergency savings means understanding the power it holds in providing a sense of security and resilience in times of need. It serves as a safety net, offering the freedom to navigate through life’s challenges without incurring detrimental consequences or having to rely on external sources for support.

The significance of having a financial buffer also lies in its ability to alleviate stress and anxiety that typically accompany financial uncertainties. With emergency savings in place, individuals can face unexpected expenses or temporary loss of income with confidence, knowing they have a reliable fallback plan to rely on.

Moreover, understanding the importance of emergency savings equips individuals with the knowledge and motivation to prioritize saving for the future. It encourages the development of responsible financial habits, such as budgeting and setting realistic savings goals, which ultimately contribute to long-term financial success.

In conclusion, grasping the significance of emergency savings empowers individuals to become proactive stewards of their financial well-being. By understanding its value, individuals can take the necessary steps to establish and nurture their own financial safety net, ensuring a more secure and stable future.

Why Everyone Should Have Emergency Savings

In today’s uncertain world, it is crucial for individuals to have a financial safety net in the form of emergency savings. Having adequate savings set aside for unexpected situations provides a sense of security and peace of mind. Whether it’s a medical emergency, job loss, or a sudden home repair, having emergency savings allows individuals to weather these storms without facing devastating financial consequences.

Safeguard Against Unforeseen Circumstances

An emergency can strike at any time without warning, and being unprepared can lead to long-lasting financial struggles. By maintaining emergency savings, individuals can protect themselves and their families from the unpredictable challenges that life throws their way. It serves as a cushion to mitigate the financial impact of unexpected events and ensures that basic needs can still be met during tough times.

Consider the peace of mind that comes with having a safety net when faced with a sudden illness or injury that requires expensive medical treatments. Emergency savings can provide the means to access the necessary healthcare without compromising financial stability.

Preserve Financial Independence

Having emergency savings is instrumental in preserving financial independence. It allows individuals to avoid relying on high-interest credit cards or loans in times of crisis, thus preventing the accumulation of debt. By being self-reliant during emergencies, individuals can maintain control over their finances and avoid falling into a cycle of recurring financial difficulties.

Imagine being able to tackle unexpected car repairs or replace essential household appliances without resorting to borrowing money or burdening oneself with additional financial obligations. Emergency savings empowers individuals to handle such situations with confidence and stability.

Opportunity to Seize Life’s Unexpected Moments

Emergency savings not only act as a safety net but also open doors to pursue unforeseen opportunities. Whether it’s starting a new business venture, taking up an exciting career change, or embarking on a once-in-a-lifetime travel experience, having savings designated for emergencies enables individuals to take calculated risks and explore new possibilities.

Consider the freedom that comes with having the financial means to take advantage of a golden opportunity. With emergency savings as a safety net, individuals can confidently pursue their dreams without the fear of bankruptcy or financial ruin.

In conclusion, emergency savings are indispensable for everyone, providing a sense of security, preserving financial independence, and allowing individuals to embrace unexpected opportunities. Starting and diligently contributing to emergency savings is a wise financial decision that ensures a brighter and more stable future.

Financial Security in Unforeseen Circumstances

In the realm of unforeseen events, establishing a sense of financial security is of utmost importance. When faced with unexpected circumstances, having a stable monetary foundation is crucial to weather the storm. While a guide on starting emergency savings may detail the significance of such preparations, it is imperative to delve into the broader scope of financial security in the face of unforeseen circumstances.

One key aspect of financial security lies in the ability to adapt and react effectively when life takes unexpected turns. Building a robust financial safety net enables individuals to handle unpredictable situations such as job loss, medical emergencies, or natural disasters without experiencing overwhelming financial hardships. By wisely allocating resources, planning for contingencies, and diversifying investments, individuals can establish a solid foundation that provides them with the necessary resilience to face uncertainties head-on.

Moreover, financial security in unforeseen circumstances extends beyond mere survival. It grants individuals the freedom to make conscious decisions, unburdened by the constant worry of uncertain financial futures. It opens doors to opportunities, whether it be furthering education, pursuing new career paths, or taking calculated risks. A strong financial backbone serves as a catalyst for personal growth and empowerment, enabling individuals to explore untapped potential and pursue their dreams.

| Benefits of Financial Security in Unforeseen Circumstances |

|---|

| 1. Peace of mind: With a solid financial foundation, individuals can enjoy peace of mind knowing they are prepared to handle unexpected events. |

| 2. Reduced stress: Financial security decreases stress levels as individuals are not constantly burdened by the fear of financial instability. |

| 3. Improved decision-making: Being financially secure allows individuals to make choices based on their passions and goals rather than solely on monetary considerations. |

| 4. Enhanced resilience: A strong financial safety net enables individuals to recover more swiftly and effectively from unforeseen events. |

| 5. Increased opportunities: Financial security creates the opportunity to seize new possibilities and pursue one’s aspirations without the fear of financial setbacks. |

To conclude, financial security in unforeseen circumstances is an essential element of overall well-being. It provides individuals with the stability and freedom to navigate unexpected events, reducing stress and offering peace of mind. By acknowledging the significance of financial security and taking the necessary steps to establish it, individuals can confidently face the unknown and lay the groundwork for a resilient and prosperous future.

Getting Started with Building your Emergency Fund

Embarking on the journey of creating a financial safety net can be a crucial step towards securing your future. In this section, we will explore the initial steps to start building your emergency fund. By establishing a solid foundation for your savings, you can prepare yourself for unexpected financial challenges and gain peace of mind.

Assessing Your Current Financial Situation

Understanding where you stand financially is crucial when it comes to building emergency savings. This section will guide you through the process of evaluating your existing financial conditions without explicitly referring to the significance of having funds set aside for unexpected situations.

Part of assessing your current financial situation involves a comprehensive review of your income, expenses, and debts. By examining these factors, you can gain a clear understanding of your financial health and identify areas of improvement or potential vulnerabilities.

Begin by evaluating your sources of income, including wages, salaries, bonuses, or any other regular earnings. Having a grasp of your income allows you to determine how much you have available to allocate towards savings in the long term.

Next, analyze your expenses, categorizing them into essential and non-essential categories. Essential expenses encompass necessities like housing, utilities, groceries, transportation, and healthcare, while non-essential expenses cover discretionary items such as entertainment, dining out, or vacations. Understanding the breakdown of your expenses helps in identifying potential areas where you can cut back to redirect funds towards emergency savings.

Another critical aspect of assessing your financial situation is evaluating your outstanding debts, including mortgages, student loans, credit card balances, or personal loans. Having a clear picture of your debt obligations allows you to prioritize repayment strategies or identify opportunities to reduce interest payments and free up more funds for savings.

Moreover, it is crucial to consider any existing financial commitments or obligations, such as supporting dependents or contributing to retirement accounts. These factors impact your overall financial situation and should be taken into account when determining how much you can realistically set aside for emergency savings.

By assessing your current financial situation comprehensively, you can establish a solid foundation for building emergency savings, ensuring you are equipped to handle unanticipated expenses or financial hardships in the future.

Setting Realistic Saving Goals

Creating achievable targets for saving money is crucial to building a solid emergency fund. By setting realistic saving goals, individuals can effectively plan and prioritize their finances to ensure they are adequately prepared for unexpected expenses or situations.

In this section, we will explore various strategies and tips to help you set realistic saving goals. Whether you are just starting to save or looking to enhance your current savings plan, these guidelines will assist you in developing a practical and sustainable approach.

Assessing Your Financial Situation

Before setting saving goals, it is important to assess your current financial situation. Evaluate your income, expenses, and debts to gain a comprehensive understanding of your financial standing. This assessment will help you determine how much you can realistically save and identify areas where you can potentially cut expenses to increase your savings.

Prioritizing Your Saving Objectives

Once you have assessed your financial situation, prioritize your saving objectives based on your personal needs and circumstances. Start by identifying your short-term and long-term financial goals. Short-term goals may include saving for a vacation or purchasing a new gadget, while long-term goals may involve building a down payment for a house or planning for retirement. By understanding your priorities, you can then allocate your saving efforts accordingly.

Setting SMART Saving Goals

When establishing saving goals, it is essential to follow the SMART criteria – Specific, Measurable, Achievable, Relevant, and Time-bound. Specific goals provide clear direction, while measurable goals enable you to track your progress. Ensure your saving goals are achievable within your current financial situation and relevant to your overall financial objectives. Finally, set a specific timeline to achieve your goals, creating a sense of urgency and accountability.

Tracking and Adjusting Your Progress

Tracking your saving progress is vital to ensure you are on the right track towards reaching your goals. Regularly review and adjust your saving plan as needed, especially when your financial situation or priorities change. Consider utilizing financial tools such as budgeting apps or spreadsheets to help you track your expenses and savings accurately.

By following these guidelines and setting realistic saving goals, you can develop a structured savings plan that will provide you with the peace of mind and financial stability to weather any emergency that comes your way.

Creating a Dedicated Emergency Fund

Establishing a specific reserve to handle unforeseen financial needs is an essential aspect of managing one’s personal finances effectively. This section will outline the importance of creating a dedicated emergency fund and provide insights into the process of setting it up.

A dedicated emergency fund plays a critical role in providing financial stability and peace of mind, especially during unexpected circumstances or emergencies. By cultivating this fund, individuals can safeguard themselves against unforeseen expenses, such as medical emergencies, car repairs, job loss, or home repairs. Having a well-funded emergency fund ensures that there is a safety net in place to prevent one from falling into debt or relying on high-interest loans.

Creating a dedicated emergency fund involves establishing a systematic approach to saving money regularly. One of the first steps is determining an appropriate target amount to save, which can vary depending on personal circumstances, such as income, expenses, and lifestyle. It is advisable to aim for a fund that covers at least three to six months’ worth of living expenses.

To build this fund efficiently, individuals should set up automatic transfers from their primary bank account to a separate account or a specified emergency fund account. This automatic savings mechanism helps in cultivating the habit of consistent saving and ensures that the funds are regularly allocated to the emergency fund.

A practical strategy is to initially focus on setting aside small amounts of money consistently, gradually increasing the contributions over time. By making small sacrifices in discretionary spending and prioritizing savings, individuals can steadily grow their emergency fund without significantly impacting their daily lives.

It is essential to keep the emergency fund separate from regular savings and checking accounts to prevent any unintentional spending. A separate account dedicated solely to emergencies ensures that the funds are readily accessible when needed, while also providing a clear distinction between regular savings and emergency savings.

| Benefits of a Dedicated Emergency Fund |

| 1. Financial Security: A well-funded emergency fund provides a sense of security and helps individuals navigate unexpected expenses without financial hardships. |

| 2. Debt Prevention: By having readily available funds for emergencies, individuals can avoid accumulating debt or resorting to costly loans. |

| 3. Peace of Mind: Knowing that there is a dedicated fund to handle unexpected financial challenges brings peace of mind and minimizes stress. |

| 4. Flexibility: An emergency fund offers flexibility and the ability to make informed financial decisions without being constrained by immediate monetary needs. |

Building Your Emergency Savings

Creating a robust financial safety net becomes a priority in uncertain times. Constructing your emergency savings facilitates peace of mind and ensures a stable financial future. This section will guide you through the process of establishing a reliable reserve that can safeguard you from unexpected expenses, job loss, or other unforeseen circumstances.

1. Enhance your savings habits:

- Allocate a portion of your income towards savings on a regular basis.

- Consider setting up an automatic transfer from your primary account to your emergency fund.

- Make a conscious effort to reduce unnecessary expenditures and redirect those savings towards your emergency fund.

2. Establish an attainable savings goal:

- Determine the amount you need to cover at least three to six months of essential expenses.

- Take into account factors like personal circumstances, job stability, and the nature of your expenses.

- Break down your target into smaller milestones to make it more achievable and trackable.

3. Explore diverse income sources:

- Look for potential side hustles or part-time opportunities to supplement your primary income.

- Investigate alternative ways to earn passive income, such as rental properties or freelance work.

- Redirect any additional earnings towards your emergency savings to accelerate your progress.

4. Prioritize debt management:

- Devise a strategy to pay off high-interest debts, such as credit card balances or loans.

- Consolidate multiple debts into a single payment to simplify the repayment process.

- Allocate a portion of your income towards debt reduction while simultaneously contributing to your emergency fund.

5. Explore investment options:

- Once you have built a solid emergency fund, consider diversified investment opportunities to grow your savings further.

- Consult with a financial advisor to assess the most suitable investment options based on your risk tolerance and financial goals.

- Continue to prioritize the stability and accessibility of your emergency savings while exploring potential investment avenues.

By following these steps and gradually building your emergency savings, you will enhance your financial security and resilience. Remember that consistency and discipline are key, and every small contribution towards your emergency fund brings you closer to a financially stable future.

Establishing a Budget and Cutting Expenses

Creating a financial plan and reducing costs play a vital role in building a solid foundation for your financial security. By developing a budget and finding ways to decrease your expenses, you can actively work towards achieving your long-term financial goals.

One crucial aspect of establishing a budget is assessing your income and expenditures. Start by examining your monthly earnings, including your salary, investments, and any additional sources of income. Next, evaluate your expenses, categorizing them into essential and discretionary costs. This analysis allows you to gain a clear understanding of where your money is going and identify potential areas to cut back.

After identifying your spending habits, it’s time to prioritize and make informed decisions about your expenses. Begin by focusing on reducing discretionary expenses, such as dining out, entertainment, or shopping. Look for alternative options or find ways to limit these costs without sacrificing your enjoyment. Consider preparing meals at home, exploring free or low-cost entertainment options, and embracing a more minimalist approach to buying non-essential items.

Additionally, scrutinizing essential expenses can also help you make significant savings. Research and compare different service providers for necessities like utilities, insurance, and telecommunications. Negotiate with your providers to ensure you are getting the best rates possible or consider switching to more cost-effective options. By actively managing these costs, you can potentially free up extra funds in your budget.

Tracking your expenses and monitoring your progress is essential to maintain financial discipline. Utilize budgeting tools or apps to help you categorize and analyze your spending habits. By regularly reviewing your budget and expenses, you can identify any areas where you may be overspending and make adjustments accordingly.

Establishing a budget and cutting expenses is an ongoing process that requires commitment and dedication. However, by taking these proactive steps, you are laying the groundwork for a more secure financial future and ensuring you have the necessary emergency savings in place to handle unexpected situations.

Automating Your Savings Contributions

Streamlining your savings journey can significantly enhance your financial preparedness. One effective approach is automating your savings contributions, which involves setting up automated transfers or direct deposits to allocate a portion of your income towards your emergency fund regularly.

By automating your savings contributions, you eliminate the need for constant manual transfers, making the process more convenient and hassle-free. Automating ensures that a fixed amount or percentage of your income is consistently redirected to your emergency savings, creating a sustainable saving habit without requiring continuous effort on your part.

With automated savings contributions, you can avoid the temptation of spending the allocated funds on non-essential expenses. Since the transfer happens automatically, it reduces the likelihood of diverting the money towards unnecessary purchases or impulsive spending.

Moreover, automating your savings allows you to prioritize your financial goals effectively. By specifying the amount or percentage to be saved, you establish a clear plan and commitment towards building your emergency fund. Whether you prefer small incremental deposits or larger contributions, automating your savings ensures that you stick to your goals consistently over time.

To get started with automating your savings contributions, consult your employer’s HR department to explore the possibility of setting up direct deposit into separate savings account specifically designated for emergencies. Alternatively, you can work with your bank to establish automatic transfers from your primary account to your emergency savings account on a regular basis.

Remember, automating your savings contributions is a proactive and efficient method to build financial security. It allows you to save consistently over time without requiring constant monitoring or additional effort, ultimately helping you achieve peace of mind and be better prepared for unexpected financial circumstances.

Exploring Supplemental Income Opportunities

Unlocking additional sources of income can provide a valuable cushion in times of uncertainty. This section delves into the exploration of various avenues for generating supplemental income, offering opportunities to boost your overall financial security.

Seeking out alternative income streams can be a strategic move to diversify your financial portfolio and increase your earning capacity. With the ever-changing landscape of the gig economy and the growing prominence of remote work, there are numerous avenues to explore. Whether it’s freelancing, starting a side business, or participating in the sharing economy, embracing these opportunities can offer both short-term financial relief and long-term stability.

Freelancing, for instance, opens up a world of possibilities to leverage your skills and expertise. By offering your services on platforms dedicated to connecting freelancers with clients from all over the globe, you can tap into a vast pool of potential opportunities. Whether you are a writer, graphic designer, web developer, or a skilled translator, freelancing platforms provide a network to showcase your talents and secure projects that align with your abilities.

Another avenue to consider is starting a side business. This option provides the opportunity to turn a passion or hobby into a lucrative venture. By identifying a market need and leveraging your unique skills or products, you can create a supplementary income stream that aligns with your interests. Starting small and gradually expanding can lead to significant financial returns and even the possibility of turning your side business into a full-time venture.

Exploring the sharing economy is yet another option worth considering. Platforms that facilitate peer-to-peer sharing of resources provide an avenue to monetize assets you already own. From renting out a spare room in your home to lending out equipment or even offering transportation services, participating in the sharing economy can help generate passive income and make the most of your existing assets.

By actively exploring supplemental income opportunities, you can not only enhance your financial stability but also gain valuable skills, expand your professional network, and discover new passions. Embracing these avenues empowers you to take control of your financial future and build a robust safety net, ensuring you are better equipped to tackle unexpected expenses.

Maintaining and Utilizing Your Emergency Fund

Ensuring the consistent growth and wise usage of your safety net in times of unforeseen circumstances is of utmost importance. This section delves into strategies to effectively manage and tap into your emergency savings, allowing you to handle unexpected expenses and maintain financial stability.

Regular Contributions and Replenishment: One key aspect of maintaining your emergency fund is making regular contributions. Continuously adding to your savings ensures that you can meet any unexpected expenses or financial challenges that may arise. It’s essential to set aside a fixed percentage of your income each month to keep your fund growing steadily.

Identifying Genuine Emergencies: While it can be tempting to dip into your emergency savings for non-essential purchases or short-term desires, it’s crucial to discern actual emergencies. Before utilizing your fund, evaluate if the expense aligns with the purpose of your savings: safeguarding against unexpected events such as medical emergencies, job loss, or significant home repairs.

Creating a Budget: Maintaining a comprehensive budget is essential for effectively utilizing your emergency savings. By accounting for your monthly income and expenses, you can identify areas where you may need to tap into your fund. Prioritize essential expenditures and aim to minimize unnecessary ones, helping you maintain a healthy balance between your savings and spending.

Seeking Professional Advice: In certain situations, seeking guidance from financial advisors can prove beneficial when it comes to utilizing your emergency savings. These professionals can provide personalized advice tailored to your circumstances, helping you make informed decisions and optimize the use of your funds.

Reviewing and Reassessing: Periodic reviews of your emergency fund are critical to ensure it remains aligned with your financial goals. Evaluate if the amount saved is sufficient to cover potential emergencies, and adjust your contributions accordingly. Additionally, reassess your fund’s purpose and consider any changes in your financial situation that may necessitate adjusting your strategy.

Keeping Emotions in Check: It is crucial to maintain a calm and rational mindset when utilizing your emergency savings. Unexpected events can be stressful, but it’s vital to avoid impulsive decisions that may deplete your fund unnecessarily. Evaluate the situation objectively, consider alternative solutions, and make informed choices to preserve the longevity of your emergency savings.

Documenting and Learning: Lastly, it is important to document any instances where you utilize your emergency fund. Keep a record of the reasons behind each withdrawal and evaluate if there were alternative ways to handle the situation. Learning from these experiences can help you refine your emergency saving strategy and enhance your financial preparedness for the future.

In summary, maintaining and utilizing your emergency savings effectively involves making regular contributions, discerning genuine emergencies, creating a budget, seeking professional advice when needed, reviewing and reassessing regularly, staying calm and rational during emergencies, and learning from your experiences. Implementing these strategies will enable you to navigate unforeseen financial challenges successfully and maintain a secure financial foundation.

Questions and answers

Why is emergency savings important?

Emergency savings is important because unexpected expenses or emergencies can arise at any time, such as medical emergencies, car repairs, or job loss. Without sufficient savings, individuals may find themselves in financial distress or even debt in such situations. Having emergency savings provides a financial safety net and peace of mind.

How much money should I save for emergencies?

The general rule of thumb is to save at least three to six months’ worth of living expenses. This sum should cover your essential expenses like rent/mortgage, utilities, groceries, and healthcare. However, the ideal amount may vary depending on your individual circumstances, such as job stability and financial obligations. It’s recommended to assess your monthly expenses and set a realistic savings goal accordingly.

What are some strategies to start building emergency savings?

There are several strategies to start building emergency savings. Firstly, you can automate your savings by setting up an automatic transfer from each paycheck to a separate savings account. This way, you won’t have the temptation to spend the money. Additionally, you can cut back on non-essential expenses and redirect that money towards your savings. Creating a budget and sticking to it can also help you prioritize saving for emergencies.

Should I prioritize paying off debt or building emergency savings?

It is generally recommended to strike a balance between paying off debt and building emergency savings. While it’s important to pay off high-interest debt to avoid accumulating more interest, it’s crucial to have some savings for emergencies. It’s advisable to allocate a portion of your income towards both debt payments and emergency savings to address both priorities simultaneously.

What if I have a low income and struggle to save for emergencies?

Even with a low income, it’s still possible to save for emergencies. Start by creating a budget and identifying areas where you can cut expenses. Look for opportunities to increase your income through side jobs or freelancing. Even small amounts saved regularly can add up over time. Consider starting with a small savings goal and gradually increase it as your financial situation improves.

What is emergency savings and why is it important?

Emergency savings refers to a separate fund of money set aside specifically to cover unexpected expenses or emergencies. It is important because it acts as a financial safety net, providing a sense of security and allowing individuals to handle financial setbacks without going into debt.

How much should I aim to save in my emergency fund?

The general rule of thumb is to save at least three to six months’ worth of living expenses in your emergency fund. However, the actual amount may vary depending on your individual circumstances such as income stability, debt obligations, and family size.

What are some tips on how to start building an emergency fund?

Start by setting a savings goal and creating a budget to track your expenses. Cut back on unnecessary expenses and redirect that money towards your emergency fund. Consider automating your savings and setting up a separate bank account specifically for emergencies. Additionally, explore ways to increase your income, such as taking on a side hustle or selling unwanted items.

What are examples of unexpected expenses that emergency savings can cover?

Emergency savings can cover various unexpected expenses, such as medical bills, car repairs, home repairs, unemployment, or sudden travel. It can also provide financial support during a job loss, natural disaster, or any other unexpected life event that requires immediate financial assistance.

Is it possible to start an emergency fund even if I have limited income?

Yes, it is possible to start an emergency fund even with limited income. The key is to start small and be consistent. Saving a small portion of your income regularly can gradually build up your emergency fund over time. Consider cutting down on non-essential expenses and finding creative ways to earn extra income to contribute towards your emergency savings.