Are you tired of feeling overwhelmed by your debts, trapped in a seemingly never-ending cycle of payments? It’s time to take control of your financial future and pave your path to debt freedom. In this comprehensive article, we will walk you through the crucial steps towards achieving financial independence, arming you with the necessary tools and knowledge to create a solid plan to conquer your debts.

Embarking on your debt payoff journey requires careful planning, determination, and persistence. By developing a foolproof debt repayment strategy, you can navigate your way towards a debt-free life, unburdening yourself from the stress and constraints that indebtedness imposes.

Revolutionize Your Health & Lifestyle!

Dive into the world of Ketogenic Diet. Learn how to lose weight effectively while enjoying your meals. It's not just a diet; it's a lifestyle change.

Learn MoreWithin the confines of this article, you will find expert guidance and valuable insights, enabling you to craft a personalized plan tailored to your unique financial situation. It’s time to take the reigns and redefine the trajectory of your financial future. Whether you’re burdened by credit card debt, student loans, or other financial liabilities, this guide will equip you with the essential knowledge and strategies required to overcome your debts efficiently and effectively.

- Creating a Reliable Strategy to Eradicate Debts

- Assess Your Financial Situation

- Evaluate your debts, income, and expenses

- Identify your financial goals

- Analyze your current budget

- Prioritize Your Debts

- List your debts from highest to lowest interest rate

- Consider the impact of different repayment strategies

- Select the most suitable debt payment method for your situation

- Set Clear and Attainable Goals

- Determine the time frame for becoming debt-free

- Breaking down your repayment goals into achievable milestones

- Establish a realistic budget to achieve your financial goals

- Questions and answers

Creating a Reliable Strategy to Eradicate Debts

In this segment, we will delve into the process of developing a solid strategy that ensures efficient elimination of debts. By implementing a deliberate approach, individuals can gradually overcome their financial burdens and pave the way for a debt-free future. This section aims to provide a step-by-step outline to guide you through this journey.

| Phase 1: Assessing Your Debts | |

| Step 1: Survey your liabilities | Identify all outstanding debts and their respective interest rates. |

| Step 2: Calculate total debt amount | Sum up all outstanding balances to determine the magnitude of your debt. |

| Step 3: Prioritize debts | Evaluate and rank debts based on interest rates, with the highest rates taking precedence. |

| Phase 2: Planning and Execution | |

| Step 4: Set achievable repayment goals | Create realistic targets and timelines for clearing your debts. |

| Step 5: Explore debt consolidation options | Consider consolidating multiple debts into one, more manageable loan. |

| Step 6: Develop a budget | Construct a comprehensive budget to allocate funds for debt repayment. |

| Step 7: Construct an emergency fund | Build a safety net to tackle unexpected expenses and avoid accumulating further debt. |

| Step 8: Implement diligent payment discipline | Follow a consistent schedule for making repayments and avoiding late fees. |

| Phase 3: Monitoring and Adjustment | |

| Step 9: Regularly track progress | Maintain updated records of payments made and adjustments in the debt balance. |

| Step 10: Evaluate and adapt the plan | Review your strategy periodically and make necessary alterations to optimize results. |

| Step 11: Celebrate milestones | Recognize and reward yourself when certain debt reduction milestones are achieved. |

By embarking on a structured method to tackle debts, individuals can regain control of their finances and achieve lasting financial freedom. Remember, consistency and discipline are key throughout this journey.

Assess Your Financial Situation

Understanding your current financial standing is crucial before creating a strategic plan to eliminate your debts. This section will help you evaluate and analyze your financial situation, providing you with a solid foundation to build your debt payoff plan.

Analyze your financial landscape:

Begin by assessing your income sources, such as your employment salary, freelance work, or investments. Identify any additional sources of income that can contribute towards your debt payoff.

Next, evaluate your expenses by carefully reviewing your monthly bills, loans, and credit card statements. Categorize your expenses into fixed costs, such as rent or mortgage payments, and variable costs, such as groceries or entertainment.

Evaluate your assets and liabilities:

Take stock of your assets, including your savings, investments, and valuable possessions. By understanding the value of your assets, you can determine if they can be liquidated to pay off your debts more quickly.

Similarly, assess your liabilities, which may include outstanding loans, credit card balances, or any other forms of debt. Understanding the full extent of your debts will enable you to prioritize the most significant ones and create an effective repayment schedule.

Consider your financial goals:

It is essential to consider your long-term financial goals alongside your debt repayment plan. Whether it’s saving for a down payment on a house, starting a business, or building an emergency fund, having clear objectives can motivate you throughout your debt payoff journey.

Remember, assessing your financial situation is an essential first step towards creating a debt payoff plan that suits your unique circumstances and paves the way for a more financially secure future.

Evaluate your debts, income, and expenses

Take a comprehensive look at your financial situation by evaluating your outstanding debts, income sources, and expenses. Understanding the full extent of your debts and the flow of your income and expenses is crucial for creating an effective debt payoff plan.

Start by examining your debts, which may include credit card balances, student loans, mortgages, and any other outstanding loans. Make a list of each debt, noting the total amount owed, interest rates, minimum monthly payments, and payment due dates. This will help you prioritize your debts and identify those with the highest interest rates or nearing payment deadlines.

Next, analyze your income sources. This can include your salary, wages, rental income, freelance work, or any other regular sources of income. Calculate your total monthly income and determine if there are any opportunities to increase it, such as taking on additional part-time work or exploring new revenue streams.

Once you have a clear picture of your debts and income, it’s time to scrutinize your expenses. Track your spending for a few months to identify where your money is going. Categorize your expenses into fixed costs like rent or mortgage payments, utilities, and insurance, and variable costs such as groceries, transportation, entertainment, and dining out. Determine if there are any unnecessary or excessive expenses that can be minimized or eliminated to free up more money for debt repayment.

| Debt | Total Amount Owed | Interest Rate | Minimum Monthly Payment | Payment Due Date |

|---|---|---|---|---|

| Credit Card Balance | $5,000 | 18% | $100 | 15th of every month |

| Student Loan | $20,000 | 6% | $200 | Last day of every month |

| Mortgage | $200,000 | 4% | $1,000 | 1st of every month |

By evaluating your debts, income, and expenses, you will have a clear understanding of your financial situation and be better equipped to develop a successful debt payoff plan.

Identify your financial goals

In order to create a successful debt payoff plan, it’s crucial to identify your financial goals. Understanding what you want to achieve with your finances will help you stay motivated and focused throughout the process. By setting clear goals, you can create a roadmap for paying off your debt and ultimately achieving financial freedom.

Start by taking some time to think about what is most important to you when it comes to your finances. Are you looking to become debt-free as quickly as possible? Do you want to save for a specific goal, such as buying a house or starting a business? Or perhaps you want to build an emergency fund to provide financial security for unexpected expenses.

It’s important to be specific and realistic with your goals. Instead of saying I want to pay off all my debt, try setting a specific amount and timeline, such as I want to pay off $10,000 of credit card debt within the next two years. By setting measurable goals, you’ll have a clear target to work towards.

Once you’ve identified your financial goals, write them down and keep them somewhere visible. This will serve as a constant reminder of what you’re working towards and help you stay motivated. You can even create a vision board or use a financial goal-tracking app to visually track your progress.

Remember, identifying your financial goals is the first step towards creating a solid debt payoff plan. With a clear vision of what you want to achieve, you’ll be better equipped to make the necessary financial decisions and stay committed to paying off your debt.

Analyze your current budget

Understanding your current financial situation is the first step towards creating an effective debt payoff plan. By analyzing your current budget, you can gain insight into your income, expenses, and spending habits, allowing you to make informed decisions about how to allocate your money towards debt repayment.

- Start by listing all your sources of income, including salaries, bonuses, and any other additional earnings.

- Next, make a comprehensive list of all your monthly expenses, such as rent or mortgage payments, utility bills, transportation costs, groceries, and entertainment expenses.

- Review your spending habits and identify areas where you can cut back or eliminate unnecessary expenses. This could involve reducing dining out, entertainment, or shopping expenses.

- Consider tracking your expenses for a month or two to get a clearer picture of where your money is going. This will help you identify any hidden expenses or areas where you may be overspending.

- Once you have a complete view of your income and expenses, calculate your monthly disposable income by subtracting your expenses from your income. This is the amount of money you have available each month to put towards debt repayment.

By thoroughly analyzing your current budget, you can gain a better understanding of your financial situation and identify areas where you can make adjustments to free up money for debt repayment. This knowledge will serve as the foundation for developing an effective debt payoff plan.

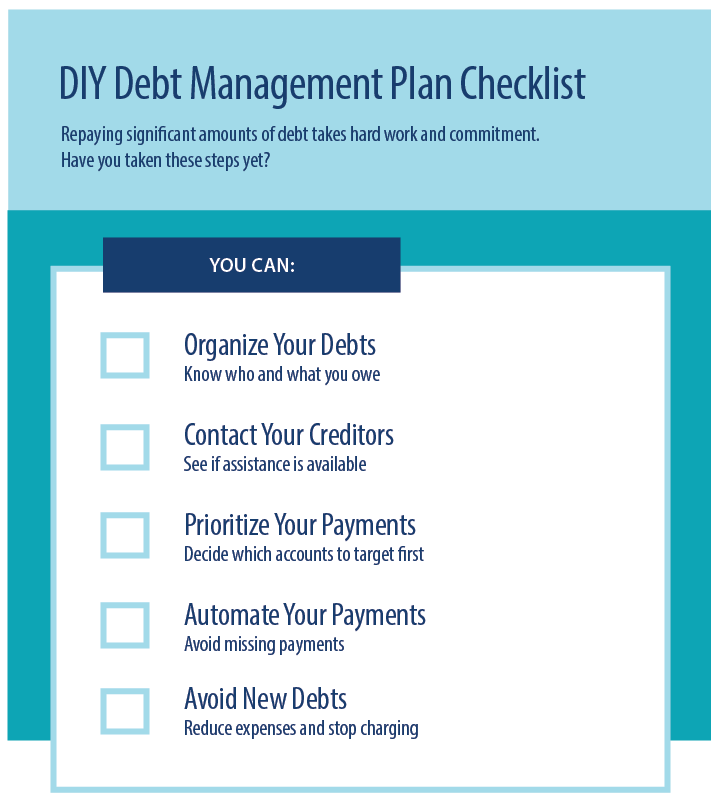

Prioritize Your Debts

When it comes to paying off your debts, it’s essential to establish a clear and effective plan. One crucial step in this process is prioritizing your debts. Prioritizing allows you to determine which debts should be paid off first based on various factors such as interest rates, outstanding balances, and potential consequences of non-payment.

An effective way to prioritize your debts is by assessing the interest rates associated with each debt. Start by identifying the debts with the highest interest rates. These debts typically accumulate more interest over time, making it costlier to carry them. By tackling high-interest debts first, you can save yourself money in the long run.

Another factor to consider when prioritizing your debts is the size of the outstanding balances. While it may be tempting to focus on smaller debts to quickly eliminate them, it’s often more beneficial to prioritize larger debts. By focusing on debts with larger balances, you can make significant progress in reducing your overall debt load.

It’s also important to take into account any consequences of non-payment. Some debts, such as mortgage payments or utility bills, may have severe consequences if left unpaid, such as foreclosure or service disconnection. These debts should be prioritized to ensure the stability of your living situation and avoid further financial hardships.

To help you stay organized and keep track of your prioritized debts, consider creating a debt repayment plan. This plan can be a simple spreadsheet or a dedicated budgeting app that allows you to list your debts, their prioritization, and track your progress as you make payments. Having a visual representation of your debts and their priorities can provide motivation and help you stay on track towards financial freedom.

- Assess the interest rates associated with each debt

- Prioritize high-interest debts first

- Consider the size of the outstanding balances

- Take into account any consequences of non-payment

- Create a debt repayment plan to stay organized and motivated

List your debts from highest to lowest interest rate

In this section, we will discuss the importance of listing your debts in order from highest to lowest interest rate. By doing so, you can effectively prioritize your debt repayment strategy and save money in the long run.

When you list your debts from highest to lowest interest rate, you can clearly see which debts are costing you the most in interest charges. This allows you to prioritize paying off the debts with the highest interest rates first, as they are the ones that are accumulating the most debt over time.

By tackling the high-interest debts first, you can reduce the overall amount of interest you pay and potentially save thousands of dollars in the process. In addition, paying off high-interest debts sooner allows you to free up more money to put towards your other debts, accelerating your debt payoff journey.

Creating a list of your debts from highest to lowest interest rate also helps you stay organized and focused on your debt repayment goals. It provides a clear roadmap for your debt payoff plan, allowing you to track your progress and celebrate milestones along the way.

- Start by gathering all the necessary information about your debts, including the current balances and interest rates.

- Organize your list by arranging the debts in descending order based on their interest rates, with the highest rate at the top.

- Take a moment to review the list and assess the impact of each debt on your overall financial situation.

- With your list in hand, you can now develop a targeted strategy for paying off your debts efficiently.

Remember, listing your debts from highest to lowest interest rate is a crucial step in creating a successful debt payoff plan. It allows you to prioritize your efforts, save money on interest charges, and stay focused on your financial goals.

Consider the impact of different repayment strategies

When creating a plan to pay off your debts, it is crucial to consider the various repayment strategies available to you. Different strategies can have a significant impact on your financial situation and the time it takes to become debt-free.

Firstly, it is important to evaluate whether you should focus on paying off your high-interest debts first or tackle your debts with the lowest balances. Both strategies have their pros and cons, and it ultimately depends on your personal financial goals and priorities. Prioritizing high-interest debts can save you money in the long run by reducing the amount of interest you pay. On the other hand, focusing on low-balance debts can provide you with a sense of accomplishment and motivation as you quickly eliminate them.

In addition to prioritization, you may also consider consolidating your debts into a single loan or credit card with a lower interest rate. Debt consolidation can simplify your repayment process by combining multiple debts into one, making it easier to manage and potentially saving you money on interest charges. However, it is essential to carefully assess the terms and conditions of any consolidation options to ensure it is a financially beneficial choice for you.

Another strategy to consider is the snowball method, which involves making minimum payments on all debts except the smallest one. By allocating additional funds towards the smallest debt, you can quickly eliminate it and gain momentum in your debt repayment journey. This approach can provide psychological satisfaction and motivation as you see tangible progress and gradually tackle larger debts.

Lastly, it is crucial to regularly reassess and adjust your repayment strategy as your financial situation evolves. Unexpected expenses, changes in income, or new financial goals may require modifying your plan to ensure it remains effective and relevant.

Overall, considering the impact of different repayment strategies is essential to create a tailored debt payoff plan that aligns with your financial goals and priorities. By carefully weighing your options and making informed decisions, you can optimize your repayment journey and achieve financial freedom sooner.

Select the most suitable debt payment method for your situation

When it comes to repaying your debts, it’s crucial to choose a repayment method that aligns with your financial situation and goals. There are various approaches you can take to tackle your debt, each with its own advantages and considerations. By selecting the right repayment method, you can effectively and efficiently work towards becoming debt-free.

Here are a few popular strategies that you can consider:

- Snowball Method: This approach involves paying off your debts from smallest to largest balance, regardless of interest rates. By focusing on clearing your smaller debts first, you can gain momentum and motivation as you see the number of debts decrease.

- Avalanche Method: With this method, you prioritize repaying your debts based on their interest rates. Start by focusing on the debt with the highest interest rate and make minimum payments on the other debts. Once the highest-interest debt is cleared, move on to the next one. This method can potentially save you money on interest payments over time.

- Debt Consolidation: Consolidating your debts involves combining multiple debts into a single loan or line of credit. This can simplify your repayment process by having only one monthly payment and, in some cases, may secure a lower interest rate. It’s important to carefully assess the terms and fees associated with debt consolidation options.

- Debt Settlement: This method involves negotiating with your creditors to settle your debts for less than the total amount owed. It can be an option for individuals facing significant financial hardship, but it may have a negative impact on your credit score. Seeking professional advice and exploring alternative options is recommended before pursuing debt settlement.

Remember, the best debt repayment method for you depends on your financial situation, priorities, and capabilities. Take the time to evaluate your options and seek guidance from financial experts if needed. The key is to choose a strategy that you can realistically commit to and that aligns with your long-term financial goals.

Set Clear and Attainable Goals

Establishing clear and attainable goals is a crucial component of creating an effective debt payoff plan. By setting specific objectives, you can outline a roadmap for achieving financial freedom and eliminating debt.

When setting goals, it is important to ensure they are realistic and feasible. Unrealistic goals can leave you feeling discouraged and demotivated, making it more challenging to stay on track with your debt repayment journey. Take into account your current financial situation, income, and expenses to set goals that are achievable within a reasonable timeframe.

Furthermore, it is essential to define your priorities and determine what matters most to you. This will help you stay focused and motivated throughout the process. Whether your goal is to become debt-free by a certain date or to pay off a specific amount of debt, clarity in your objectives is key.

- Be specific: Instead of setting a vague goal like pay off debt, define the exact amount you want to pay off and the timeframe you aim to achieve it in.

- Break it down: Divide your overall debt goal into smaller, more manageable milestones. This will provide a sense of progress and keep you motivated along the way.

- Track your progress: Regularly monitor your progress towards your debt payoff goals. This will enable you to make adjustments if necessary and celebrate your achievements along the way.

- Stay flexible: Remember that circumstances can change, and it is important to adapt your goals accordingly. Allow some flexibility in your plan to accommodate unexpected expenses or changes in income.

In summary, by setting clear and attainable goals, you can create a solid foundation for your debt payoff plan. Clear goals will provide you with direction and motivation, ensuring that you stay on track and ultimately achieve financial freedom.

Determine the time frame for becoming debt-free

Planning is essential when it comes to becoming debt-free. One of the key components of creating a successful debt payoff plan is determining the time frame in which you aim to become debt-free. Setting a specific time frame provides you with a clear goal to work towards and helps you stay motivated throughout the process.

- Start by assessing your current financial situation and evaluating the amount of debt you need to pay off. Take into consideration the total amount owed, including the principal amount and any interest or fees that may accrue over time.

- Consider your monthly income and expenses to determine how much you can realistically allocate towards debt repayment each month. This will help you establish a budget and identify any areas where you can cut back on expenses to free up additional funds for debt repayment.

- Based on your available funds and the total amount of debt, calculate how long it will take to become debt-free. Divide the total debt by the monthly amount you can dedicate to repayment to determine the number of months or years it will take to pay off the debt completely.

- Keep in mind that unforeseen circumstances may arise during the repayment process, such as unexpected expenses or changes in income. It is important to build some flexibility into your plan to account for these situations and adjust your timeline if needed.

By determining the time frame for becoming debt-free, you can create a realistic and achievable goal that will keep you focused and motivated. Regularly track your progress and make adjustments as necessary to ensure you stay on track towards your desired debt-free future.

Breaking down your repayment goals into achievable milestones

Creating a plan to pay off your debt can feel overwhelming, especially if you have a significant amount to repay. However, by breaking down your repayment goals into manageable milestones, you can make the process more approachable and attainable.

Instead of focusing on the big picture and feeling discouraged by the magnitude of your debt, it’s important to break it down into smaller, more digestible targets. By setting achievable milestones, you can track your progress and stay motivated along the way.

Start by assessing your current financial situation and determining a realistic timeline for debt repayment. Consider factors such as your income, expenses, and any upcoming financial commitments. This will help you establish a timeline that fits your individual circumstances.

Next, divide your total debt into smaller chunks or milestones. You can focus on paying off one credit card or loan at a time, for example. This approach allows you to concentrate your efforts on a specific debt, making it easier to measure your progress and celebrate your achievements.

Consider prioritizing your debts based on interest rates or balances. It may be beneficial to tackle debts with higher interest rates first to minimize the amount you ultimately pay in interest. Alternatively, you may choose to start with smaller debts for a sense of quick accomplishment, known as the snowball method.

Remember to regularly evaluate your milestones and adjust them as needed. As you make progress, you may find that you are able to pay off your debts more quickly than anticipated. Celebrate these achievements and consider setting new milestones to keep yourself motivated.

In conclusion, breaking down your repayment goals into manageable milestones is an effective strategy for paying off debt. By setting achievable targets, assessing your financial situation, and prioritizing your debts, you can stay focused and motivated throughout your debt repayment journey.

Establish a realistic budget to achieve your financial goals

In order to effectively manage your debt and work towards becoming debt-free, it is essential to establish a realistic budget. A budget serves as a roadmap for your financial journey, allowing you to allocate your income and expenses in a way that aligns with your goals.

Creating a budget requires assessing your current financial situation and determining how much money you have coming in and going out each month. It involves carefully evaluating your income sources, such as salary, bonuses, or side hustles, and identifying your fixed expenses, such as rent, utilities, and loan payments.

Once you have a clear picture of your income and fixed expenses, it’s important to consider your variable expenses. These can include discretionary spending on entertainment, dining out, shopping, and other non-essential items. It’s essential to be honest with yourself and differentiate between needs and wants to establish a budget that allows for both saving and debt repayment.

While creating your budget, it’s crucial to prioritize your financial goals. Whether you want to pay off your debts, save for emergencies, invest for the future, or achieve other milestones, understanding your priorities will help you allocate your resources accordingly. Consider setting short-term and long-term goals, and establish milestones to track your progress.

Remember, creating a budget is not a one-time activity. It requires regular review and adjustments to accommodate changes in your income, expenses, and financial goals. Make sure to track your expenses diligently and compare them against your budget to identify areas where you may need to cut back or reallocate funds.

In conclusion, establishing a realistic budget is an essential step towards achieving your financial goals and becoming debt-free. By carefully evaluating your income, fixed expenses, and variable expenses, and aligning them with your priorities, you can create a budget that sets you up for success. Regular review and adjustments will ensure that your budget remains effective and supports your journey towards financial freedom.

Questions and answers

What is a debt payoff plan?

A debt payoff plan is a strategic approach to paying off debt, which involves creating a structured plan to systematically eliminate outstanding debts.

Why is it important to have a debt payoff plan?

Having a debt payoff plan is important because it provides a clear path and roadmap for paying off debts, helping individuals stay organized, motivated, and focused on achieving their goal of becoming debt-free.

How do I create a debt payoff plan?

To create a debt payoff plan, you first need to determine your total outstanding debt, prioritize your debts, set a target date for debt repayment, allocate a monthly budget towards debt repayment, and consider using debt payoff strategies such as the snowball or avalanche method.

What are the benefits of using the snowball method for debt payoff?

The snowball method for debt payoff involves paying off the smallest debts first, followed by gradually tackling larger debts. The benefits of this method include building momentum and motivation by quickly eliminating smaller debts, as well as freeing up more funds to put towards larger debts as the smaller ones are paid off.

How long does it take to become debt-free with a debt payoff plan?

The time it takes to become debt-free with a debt payoff plan varies depending on factors such as the amount of debt, the individual’s income, and the chosen debt payoff strategy. With dedication and consistent effort, it is possible to become debt-free within a few years.

What is a debt payoff plan?

A debt payoff plan is a systematic approach to getting out of debt. It involves creating a strategy to pay off outstanding debts in a timely and efficient manner.

Why is it important to have a debt payoff plan?

Having a debt payoff plan is important because it allows individuals to take control of their finances and work towards becoming debt-free. It helps in reducing interest payments and improving financial stability.

Which debt repayment strategy should I choose?

The choice of debt repayment strategy depends on individual preferences and financial circumstances. The snowball method focuses on paying off debts with the smallest balance first, while the avalanche method prioritizes debts with the highest interest rate. It is important to evaluate each strategy and choose the one that aligns best with your goals and motivations.

How long will it take to pay off my debts?

The time it takes to pay off debts depends on various factors such as the amount of debt, interest rates, monthly payments, and additional funds available for repayment. By using a debt payoff calculator and consistently following your debt payoff plan, you can estimate a timeline for becoming debt-free.